Aggregators: Who are you?

February 2018

Should renewable projects be suspicious about this friendly looking player that just arrived in the industry?

In this last chapter of our series covering the French renewables’ market entry (see here blogs 1/3 and 2/3), let’s focus on the newcomers: the aggregators.

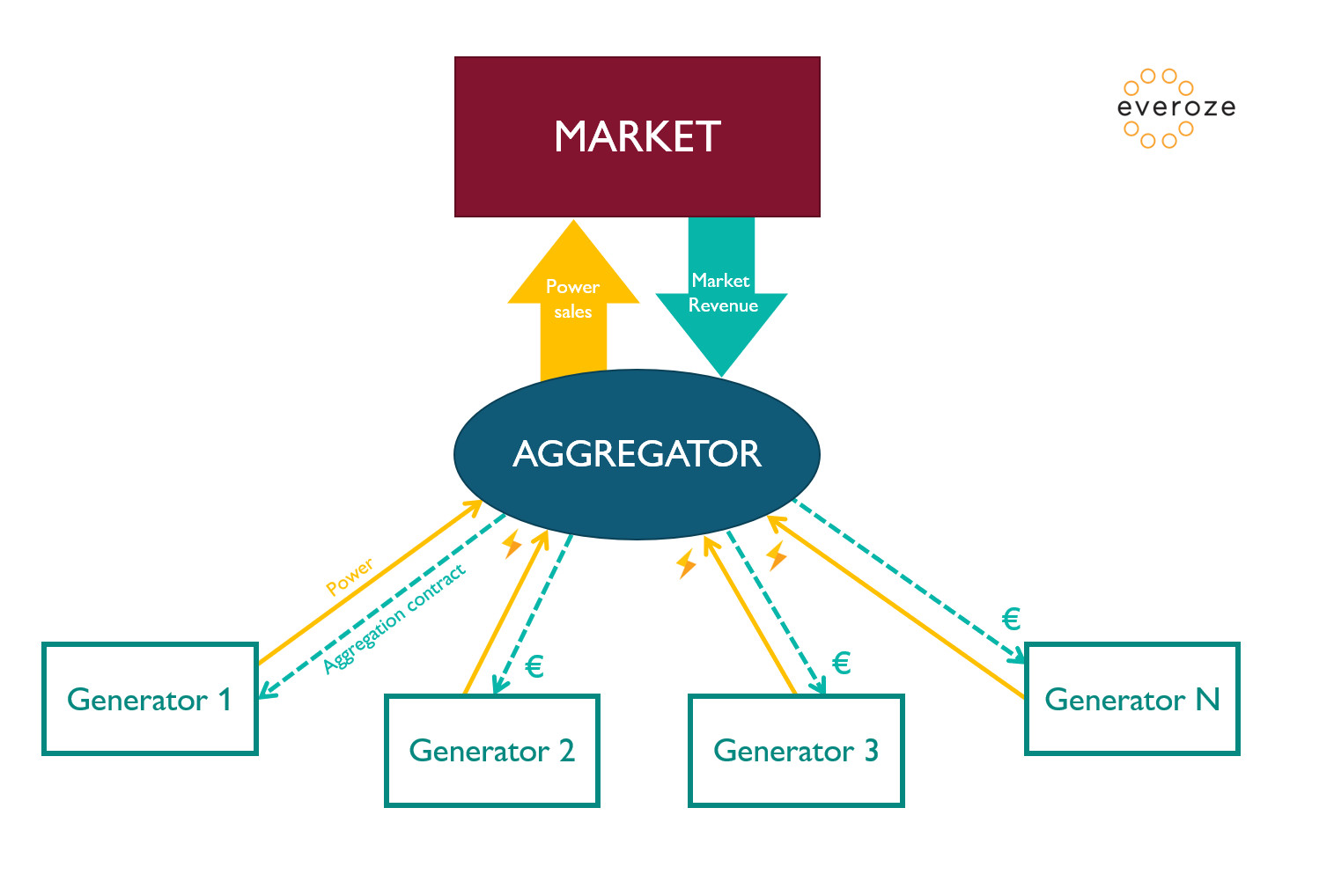

Whether it is an internal capability or not, the clear majority of power generators willing to sell their production on wholesale markets will call upon an aggregation service. In addition to being the market agent for the power producer, the aggregator will, above all, help them sell their production at the best price and mitigate balancing risk.

Before raising the issues that may result from aggregation services for French renewables, it is important to understand how aggregators fulfill their mission.

Aggregators, generators’ sales representative

Generally speaking, and ignoring the capacity market, aggregation contracts will consist in guaranteeing an electricity sales price profile for the producer in exchange of a service fee (per sold MWh).

The case gets complicated considering that trading electricity has some specificities:

- Offer-demand balance is a real-time technical necessity, which cannot be directly translated within wholesale market transactions. Auctions are organised with a relatively high frequency (typically an hourly basis) but with some anteriority (a few minutes to several hours). The inevitable discrepancies between the volumes sold beforehand and the effective production are financially penalised by the grid operator.

- Power generation characteristics are never constantly under control. It can be driven by fluctuating variables:

– Fuel price volatility, e.g. natural gas, coal, …

– Production output variations, e.g. wind, solar, hydro, …

How can aggregators manage to sell efficiently their clients’ output on an hourly basis, while limiting deviations, considering they do not know in advance the production volumes and costs of their clients?

In fact, aggregators are not totally blind. They will indeed devote important resources on predicting:

- Market prices

- Production costs (fuel price predictions)

- Production volumes (short-term forecast models for wind and solar plants)

These models give the aggregators estimations of the key parameters of the market, helping them formulate their bids.

But it does not stop here. Since predictive models come with some uncertainties, the generator’s selling sheet is still not safe from deviations and therefore penalties. Basically, the lower the uncertainties, the lower the balancing risk and the higher the competitiveness.

To reduce uncertainties, aggregators have another lever to pull-on: aggregation! Indeed, trading together various power sources can reduce the global uncertainty of the prediction models as long as these sources are physically independent. That is why a large and diverse portfolio (mixing renewables and dispatchable power sources) will help the aggregator optimise the sales of its clients by reducing the related penalties.

So, focusing back on French renewables, for which aggregators are brand-new players, is there anything to worry about?

After working on several projects in 2017, here’s the Everoze view on the two main risks associated to this service:

- Aggregation’s influence on plant operation

- Aggregation contracts’ sustainability

The aggregator, a new decision maker for renewable plant operation?

For French renewable power projects which will have to enter the market, the aggregator fits in as a new link in the value chain. This link will not only have an impact on the revenue from the marketing side, but also on the operation side. In most cases, the aggregator will request some space in the operational control hierarchy of the project. Indeed, in order to optimise trading operations, plant disconnection may be requested, either to limit deviations, or to react to negative prices.

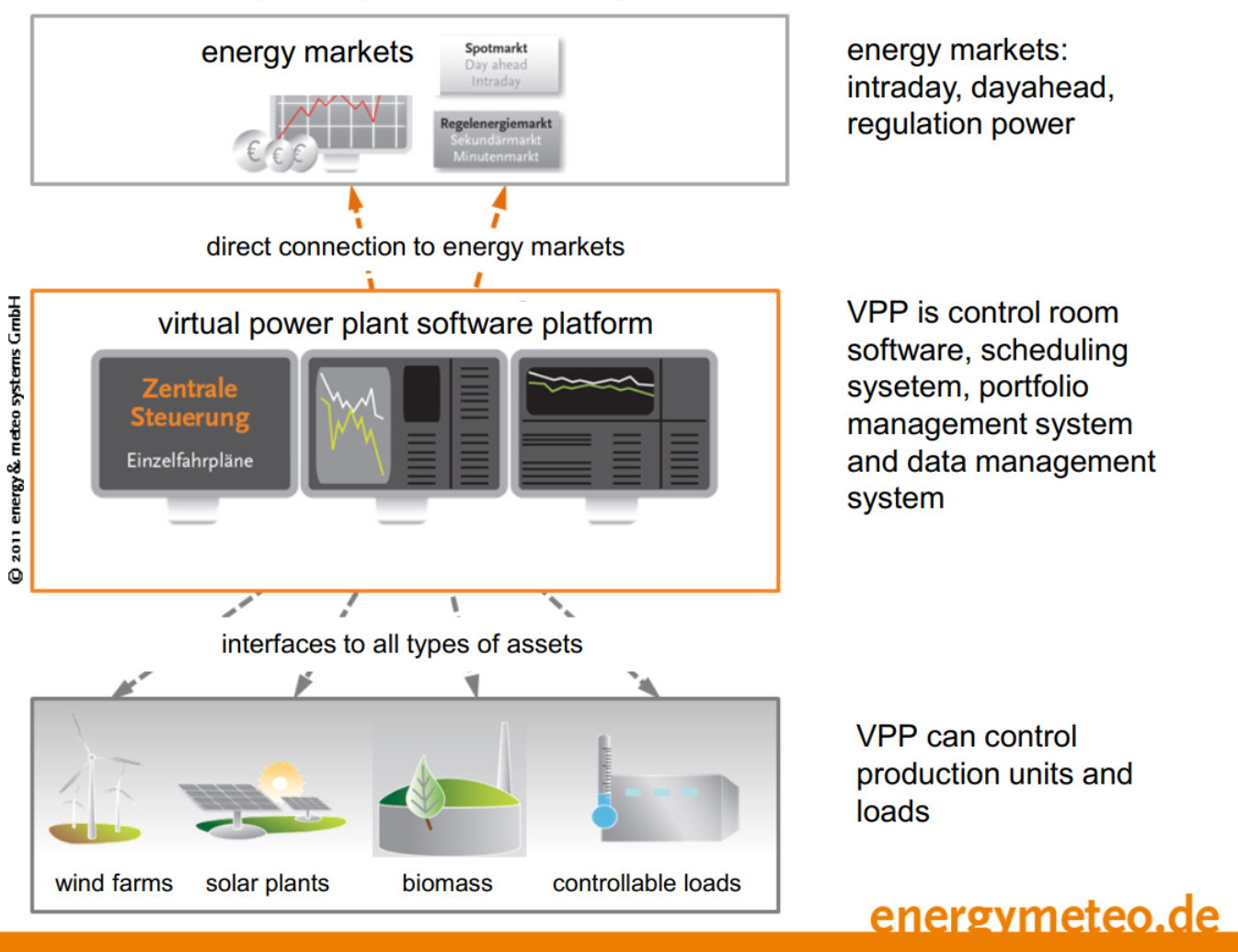

In practical terms, this has to be defined precisely within the aggregation contract to secure the decision-making and technical control chain in this respect. State of the art aggregation services consists in building a virtual power plant (VPP) with remote control on each individual plant, as in the following diagram [1]:

The main consequence of this new hierarchy relies on the operation and maintenance of the plant. As a matter of fact, maintenance operations will have to take into account these new market effects and the associated orders coming from the aggregator. Although these instances will be limited (peak hour periods related to the capacity market for example, c.f. our first blog) implications can extend to the O&M provider and therefore provisions should be included as clearly as possible within maintenance contracts.

In the same vein, Everoze recommends further discussions between the different players (owner, maintenance operator, aggregator, …) to define how to share the risk of shortfall due to negative-price curtailment.

Aggregation contracts, only a short-term perspective?

The second risk Everoze identifies with aggregation services is specific to the current context in France, namely a fierce competition!

It is quite easy to understand why aggregators are positioning aggressively in the French market of renewables:

- As described previously, aggregators have a strategic interest in having large and diverse portfolios to improve their competitiveness

- Two large populations of projects are starting to need aggregation services at the same time

– New projects, under the new CfD regime

– Older projects coming to the end of their FiT contracts

Such a highly competitive context puts aggregators in an uncomfortable position by pushing them to proposing aggressive contract terms in order to build an efficient portfolio which is necessary to survive.

Two main risks can be associated to this particular context:

- Counterparty risk. Everyone might not survive in the French aggregation jungle. Better check how the service provider is backed financially, without such the project might end up having to find a new provider at some point.

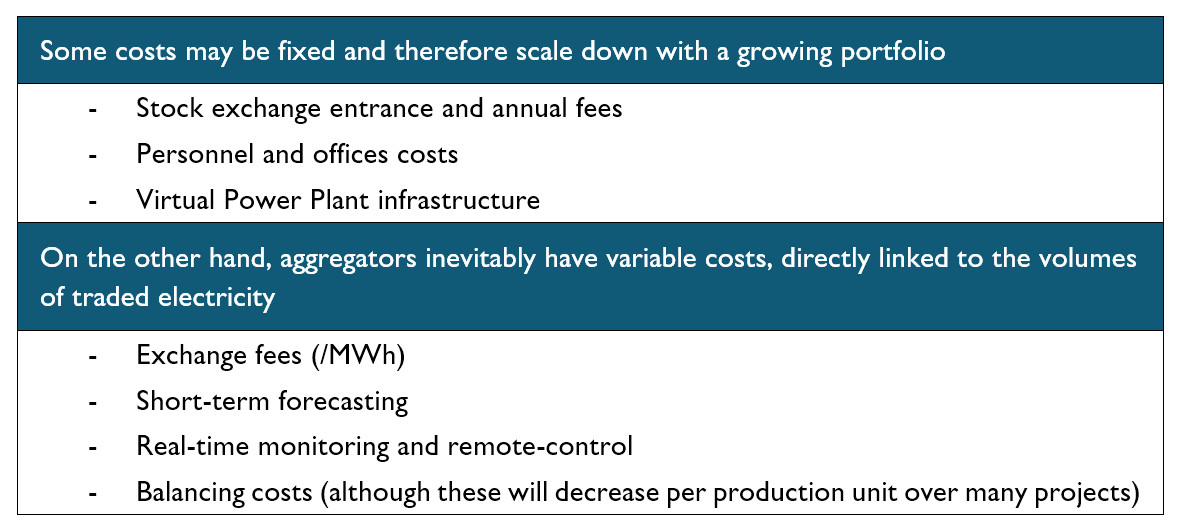

- Contract pricing increase. To attract generators and build their portfolio, aggregators may be tempted to propose low price contracts for a start. However, they actually do have running costs to operate their service.

On the other hand, some players anticipate continuous aggregation costs reduction due to generation portfolios’ growth (in size and diversity), short term prediction improvements, increasing market liquidity and broader market integration at the European scale.

Given 2017’s experience and discussions, Everoze considers both scenarios (aggregation prices increase vs decrease) as possible. Our sole conviction is that uncertainties currently remain in this regard.

Obviously, lack of visibility on the aggregation costs added to a counterparty risk, may at the start lead to some concern for renewable energy projects.

Keep calm and adapt

At the end of the day, concern about aggregation arises from the impossibility of securing a sound and stable service on the long-term, mainly considering pricing aspects.

But isn’t it what the market entry of French renewables is all about? The transition has already taken place in some neighbouring countries (Spain, Germany, …). This shows that:

- Renewable technologies are mature enough to enter the market, technically and economically.

- Renewable power enhances market liquidity by increasing volumes traded on day-ahead and intraday platforms. As a result, global balancing costs of the system are reduced [2].

———————————————————————————————————

[1] Source: Energy&Meteo Systems

[2] This is found to be true for current levels of renewable power penetration in Europe, i.e. up to 30-35%.