How 2021 could be the year that oil and gas majors crack the offshore wind industry

Published December 2020

With 2020 coming to an end, Everoze partner Graeme Wilson reflects on some interesting trends and developments that we have observed in the offshore wind industry during the past 12 months, and he makes some bold predictions as to what this may mean for 2021…

Oil and Gas Majors Become Offshore Wind Pace-setters

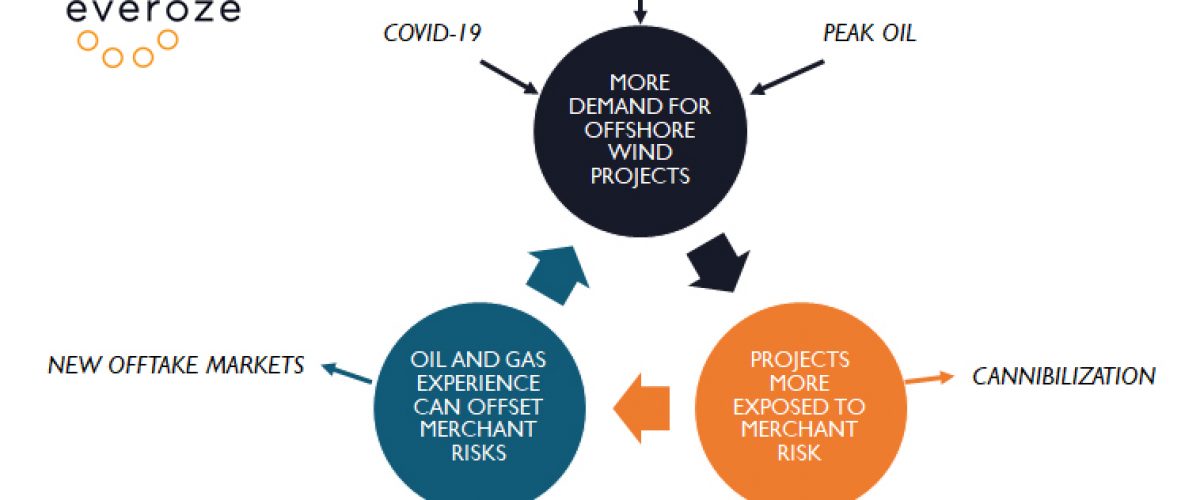

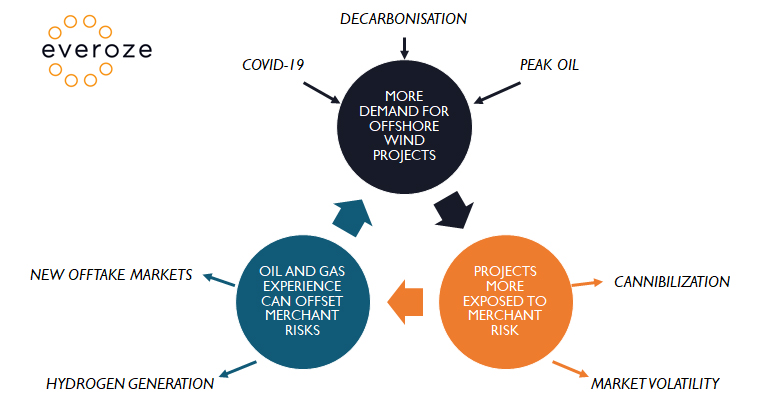

It is well documented that Covid-19 has accelerated the decline of the oil and gas industry and as a result of this and wider market trends, oil and gas majors have been increasingly active in the offshore wind industry in 2020. Offshore wind offers oil and gas players synergies with their existing activities, a place to invest large volumes of capital for a long time and also a very public way of decarbonising.

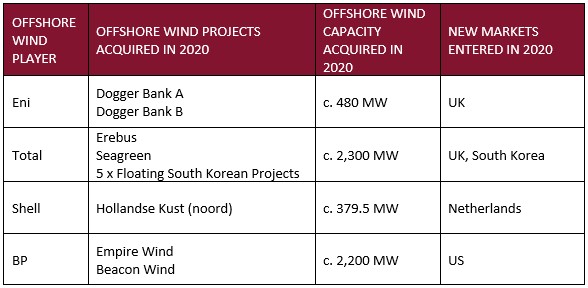

In addition to oil and gas major Equinor, an established incumbent in the offshore wind industry, this year has seen the announcements of partnerships, acquisitions and lease awards for BP, Shell, Total and most recently Italian oil and gas giant, Eni. Over 5 GW of capacity has been acquired in 2020 by these companies, who have traditionally focused on oil and gas.

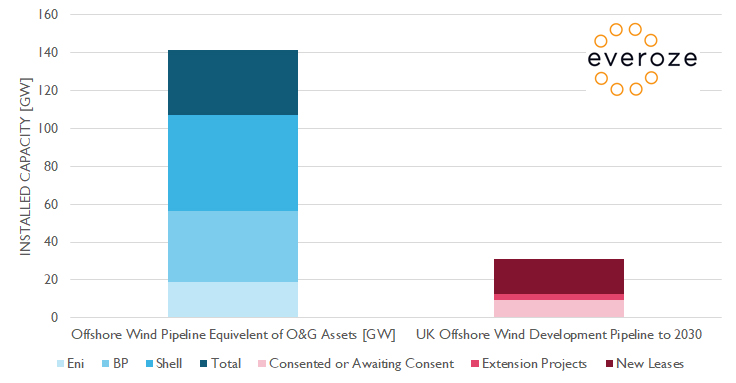

Despite this progress and some clear statements of intent, the relatively small size of the offshore wind market and considerable competition in securing equity are still significant hurdles for oil and gas companies, who’s existing portfolios of fossil fuel assets are worth several orders of magnitude more than the entire current offshore wind development pipeline. The total value (as of 2019) of assets belonging to the oil and gas majors above is approximately $1.1 trillion. If the oil and gas majors were to convert all of these assets into offshore wind farms (assuming a price of £6m / MW), it would require an available capacity of approximately 140 GW. In the UK the pipeline to 2030 is currently estimated to be around 30 GW.

This is, of course, a very simplistic illustration. But it does show why the available projects are fought over so aggressively. It is also important to bear in mind that for all the successful acquisitions secured by those above, these players (and several others who are yet to land a project) have likely failed in many other transactions. Pension funds and traditional infrastructure investors are also keen to secure these assets and are due to covid-19 and decarbonisation, also aggressively pursuing projects.

The pressure on oil and gas majors to secure a stake in the offshore wind industry quickly is obvious. With every deal that passes the valuations get higher, the pool of interested parties gets larger, the technical challenges and risks increase as projects move into more challenging environments, the vendor business cases get ever more complex and aggressive, the oil and gas market pressures continue to build and the missed opportunities to gain valuable experience mount up.

The developer premium and transaction costs required to buy into these projects will eat into their profits, while the lack of control which often comes when holding a minority or 50:50 stake in a project which will be constructed and operated by a potential future competitor, is a price the oil and gas majors will only pay for so long. They must eventually decide to assert themselves and go it alone.

To achieve anything even remotely close to the double-digit profit margins they’re used to, I suspect the long-term strategy of many of these oil and gas majors will be to vertically integrate themselves into the market. By doing this they could achieve competition-beating low prices by both managing and carrying out the construction activities themselves, before bringing O&M in-house utilising their considerable engineering and logistics capabilities. The purchase of Dogger Bank A and B by Eni – who also own Saipem, an established oil and gas EPCI contractor and also the project’s offshore substation T&I contractor – may be the start of a trend where we see other projects owned and constructed by oil and gas majors.

Merchant offshore wind is here and oil and gas are well placed to exploit it

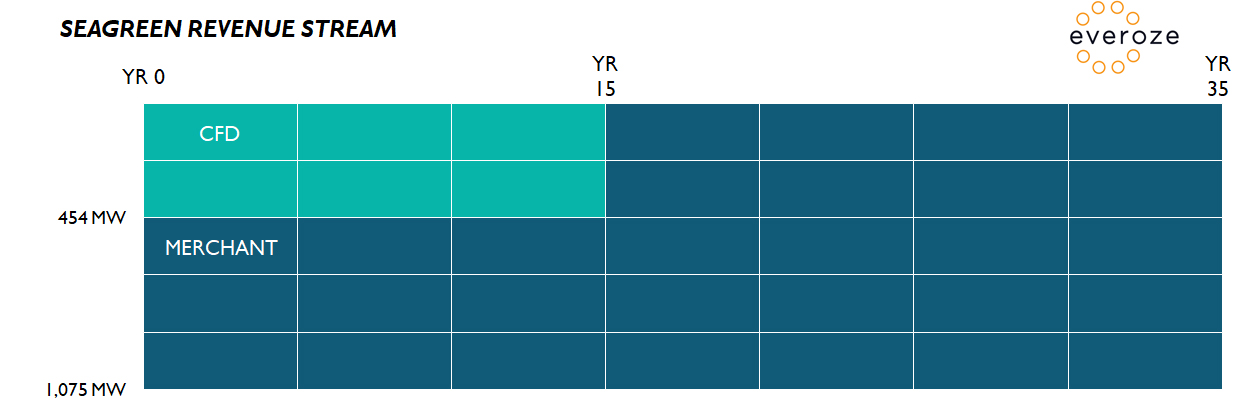

2021 may be a decisive year in the future of merchant offshore wind projects in the UK. Seagreen demonstrated earlier this year, that a partially merchant project is bankable and has a route to market, even amidst a global pandemic.

Of the 1,075 MW installed capacity at Seagreen, just 454 MW will be supported by CfD. This means, that if the project operates for 35 years, only 18% of generation will be supported by CfD (illustrated below). Seagreen has a slight advantage over projects further south as during its merchant phases it should suffer less from cannibalization in future and therefore have a higher capture price when compared to projects in the more concentrated Humber and East Anglia clusters. It is nevertheless a significant achievement.

Allocation round 4 (AR4), scheduled for Q3-2021, has a capacity cap of 12 GW, more than sufficient for the current offshore pipeline. However, this cap will be split across multiple technologies, including solar PV and a large portfolio of Scottish onshore wind projects. Due to the current high demand for offshore projects from both oil and gas and the wider investment community, some offshore projects may – like Seagreen – hedge their bets and make a second bid into AR4 for only some of their project’s total capacity and build the remaining capacity subsidy-free.

The extension projects will be particularly interesting in this regard, as they are relatively small projects which will be built close to shore and will benefit from the experience, scale, existing resource and facilities of their neighbouring projects. These projects may have a route to market without subsidy, due to the low technical and commercial risks.

An increase in merchant projects in 2021 will likely lead to more productive and meaningful discussions about alternative offtakes and new technologies to mitigate the impact of price volatility and cannibalization. Interestingly, this is where oil and gas majors again may see an opportunity.

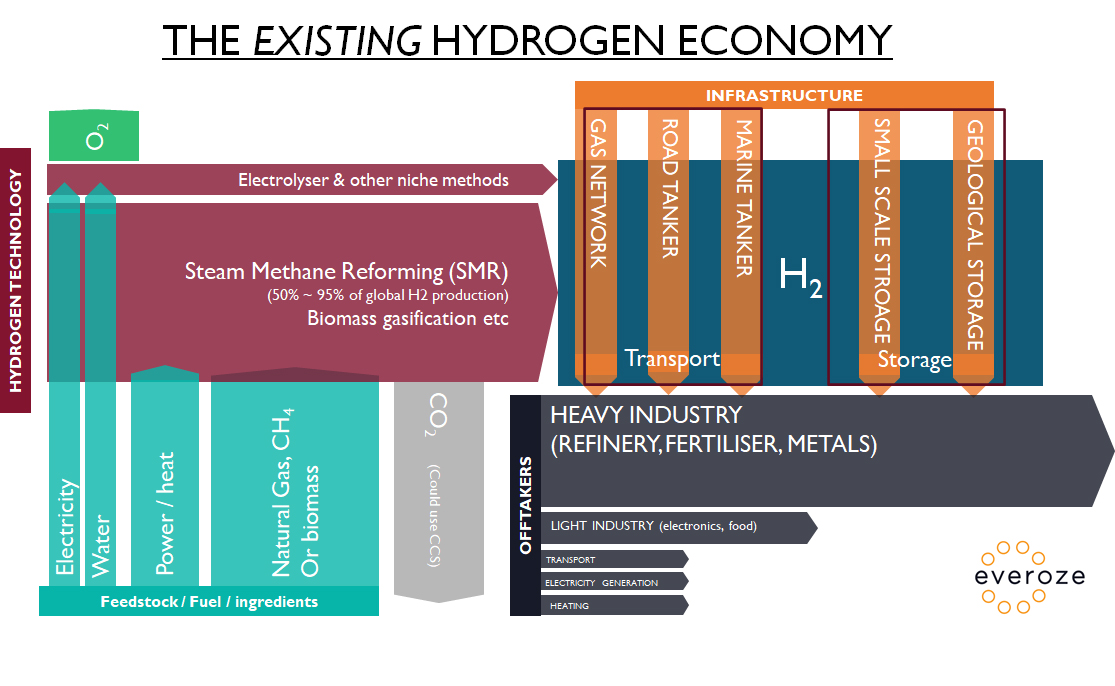

As well as being a significant year for offshore wind, there has also been a lot of hype about hydrogen. Converting the world’s existing hydrogen demand from brown (i.e. using carbon-intensive methodologies such as steam methane reformation) to green hydrogen, would require approx. 3,600 TWh of energy, or 800 GW of offshore wind. This market could therefore provide the additional offshore wind pipeline that oil and gas desperately need for further decarbonisation.

Oil and gas majors currently manufacture a significant volume of brown hydrogen for the existing hydrogen economy and therefore have valuable strategic, market and technical knowledge on the infrastructure challenges that conversion to green hydrogen would require. This may provide them with an advantage over incumbent offshore wind developers when forming their merchant business cases.

Oil and gas majors currently manufacture a significant volume of brown hydrogen for the existing hydrogen economy and therefore have valuable strategic, market and technical knowledge on the infrastructure challenges that conversion to green hydrogen would require. This may provide them with an advantage over incumbent offshore wind developers when forming their merchant business cases.

Oil and gas majors know for example the current downstream users for hydrogen, which is currently made up most significantly by heavy industry. They also have the engineering know-how needed to solve the transport and storage issues that green hydrogen will create. There is, therefore, a

significant long-term opportunity for them to expand their vertical integration strategy not just to include the development, construction and operation of offshore wind farms, but also the offtake of green electricity from their offshore wind assets to manufacture, store and transport green hydrogen to their existing heavy industry customers.

Uncertainty brings significant potential for disruption to the incumbent developers

There will be two separate leasing competitions in the UK in 2021, England & Wales and Scotwind. The processes are both different and may favour two different types of winning developers. In both cases however, there is likely to be some disruption to the status quo.

Seabed in England & Wales will simply be awarded to those who are willing to pay the most money for their respective site. This means that the winners in England & Wales will be those with the biggest bank balance, the lowest cost of capital and the grandest ambitions. My prediction for England & Wales is that, unsurprisingly, we will see some oil and gas majors walk away with the leases, as well as the largest incumbant developers.

Scotwind is a more complicated and interesting process for a variety of reasons. After a project wins lease, it will then compete for subsidy with projects in England & Wales who have better grid infrastructure, less prohibitive transmission network costs and easier seabed to build on. In their favour, however, the Scotwind sites have better wind resource and will be less impacted by price cannibalization during their merchant periods.

The other advantage they have is that they won’t necessarily have to recoup the same magnitude of the bid offer for lease as those projects in England & Wales. This is because, in the Scotwind process, the size of the lease offer is only one part of the overall bid which also considers the benefit to Scotland as a whole through the supply chain, jobs, community schemes and significantly through the development and adoption of new technology, such as the manufacturing of green hydrogen.

Despite the usual players being involved and likely remaining favourites to win seabed leases, there is the potential for some shock winners and losers in the Scotwind process. Interestingly, should any small developers win lease they will likely look for partners to help build their wind farms. Oil and gas majors would be ideal partners to buy into these projects due to the prevalence of floating sites in Scotland and also the hydrogen element – both of which are new technologies which they have more experience with than many UK utilities.

Oil and gas majors may also bring a new perspective to offshore wind. Although they won’t get the same double-digit returns in offshore wind which they are used to in oil and gas, thanks to their scale and experience, they may feel comfortable to take a more risky and aggressive procurement strategy more aligned with a multi-contract approach. Incumbent developers in the UK and Northern Europe have typically settled for less risky approaches more aligned to the EPCI model. Oil and gas majors, however, bring significant project management experience with them to the table.

The upcoming lease awards in England and Wales and in Scotland in 2021 will therefore be the first opportunity for oil and gas to seriously make their mark in offshore wind project development and it will be interesting to see how the incumbent utilities in the UK, who have had this market to themselves in recent years, react or pre-empt this move.

Summary

To summarise, my prediction for the offshore wind industry in 2021 is that we will see more merchant offshore wind projects and more oil and gas involvement in the industry. As described above, this will be driven by the following cycle:

- Oil and gas majors and other investors require a bigger pipeline of projects to buy into and develop – the demand for offshore wind projects continues to increase;

- These projects can’t all be developed with CfD and some will be merchant or will have an element of merchant risk in early years – they will therefore be subject to price volatility and cannibalization;

- More merchant projects will drive the demand and focus on alternative offtakes and new technology to offset the long-term financial impact of cannibalization and price volatility – oil and gas majors have experience of this technology and will seek to capitalise.