Synthetic Corporate PPAs: what in the world are they!?

August 2018

Have you been hearing about synthetic PPAs a lot recently, but are not really sure what it is all about? Trust me, you’re not the only one!

Have you been hearing about synthetic PPAs a lot recently, but are not really sure what it is all about? Trust me, you’re not the only one!

In my last post we saw a snapshot of the synthetic C&I PPA model along with two other C&I PPA models –private wire and sleeved PPAs. If you are not familiar with these models, I suggest you give this a read first.

Synthetic PPAs, otherwise known as Virtual PPAs or VPPAs, have been popular in the U.S. in recent years. They are now starting to gain traction in Europe – for example in the Iberian market where a few utilities are providing synthetic PPA offerings. However outside of a few key markets this structure is yet to take off in any real sense.

A key concern of these structures in the past has been the traceability of the renewable credits and ability to demonstrate the offtaker’s green credentials, as there is no physical transfer of energy between the parties. The recent changes in the policy governing Guarantees of Origin (GOO) certificates as agreed in the recast of the Renewables Directive, is helpful in the regard, and will help with the uptake of Corporate PPAs. But this will need to be followed through by the member states to ensure that the national GOO certificates mechanism is clear, the ‘unbundling’ of the energy and GOOs is not affected and any GOOs transferred are traceable and remain valid.

Not everyone agrees with the changes made in the Renewables Directive though – the revoking of GOOs for projects already receiving subsidy support proving a particularly thorny subject – but let’s save that for another day!

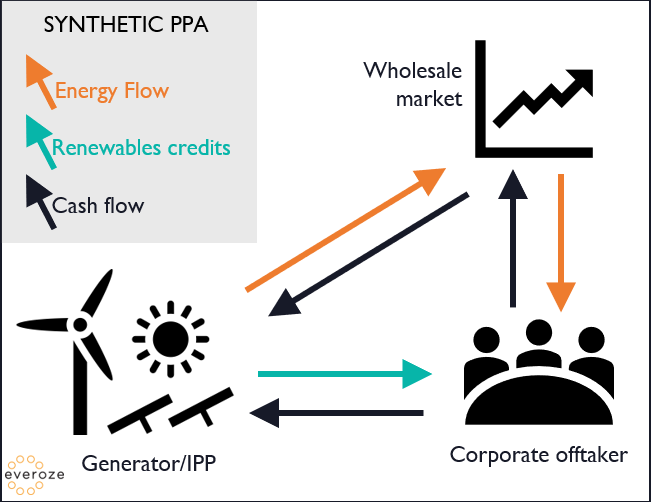

Before we go any further, for the uninitiated, a synthetic PPA is in essence a price hedging instrument – it is purely a financial contract and does not govern anything to do with the energy trading functions. The renewable generator will sell and the corporate off-taker will buy energy directly in the wholesale market. Separately, the parties will enter into a Synthetic PPA contract that provides price security against the market price for both the renewable generator and the corporate off-taker.

This structure is not very different from that adopted for projects in the UK that hold a Contract for Difference agreement with the Low Carbon Contracts Company, and the reformed subsidy mechanisms in markets like France and Ireland.

As the commercial agreement does not include any of the complex energy trading provisions and the parties’ risk allocation, negotiations tend to be simpler and focused on just a handful of key commercial points.

As synthetic PPAs are essentially financial instruments, derivative contract structures such as swaps and options are typically used for synthetic PPAs. The nature of these contracts lends itself to be better suited for standardisation, compared to the sleeved and private-wire structures. There has been some discussion on the adoption of the ISDA Master Agreement, which is commonly used for over-the-counter derivatives transactions in the financial sector, for structuring synthetic PPAs. If made to work, this will drastically reduce contract drafting efforts and time to contract.

Now, a quick word on swaps and option structures:

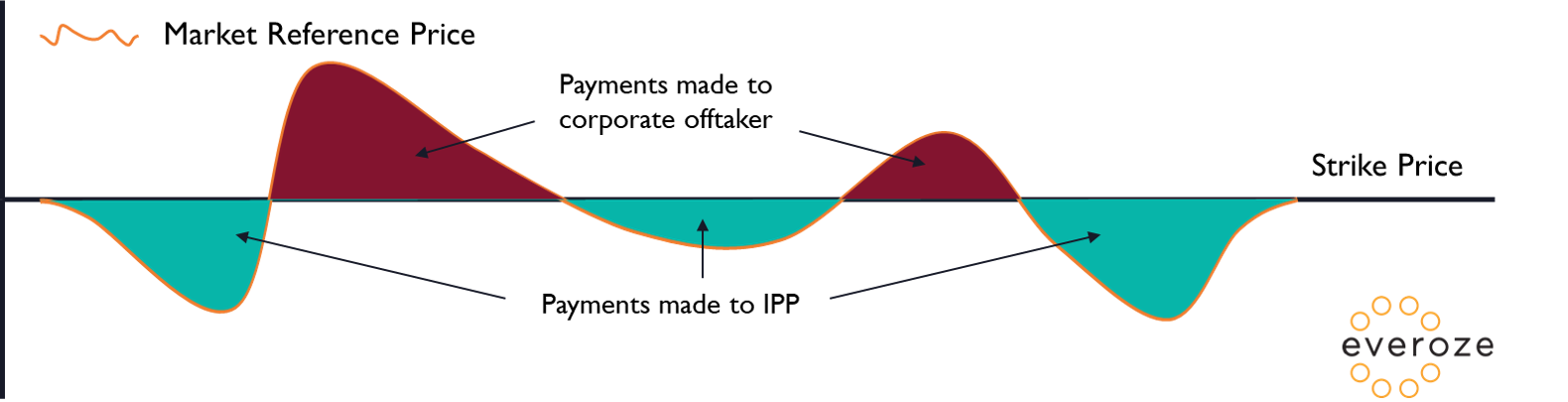

Swaps or Contract for Difference

A swap is basically a Contract for Difference which is a term many in the renewables industry have come to be familiar with now. Parties agree on a ‘strike price’ as the basis for the swap for energy delivered, where if the day-ahead market price (or any other reference price) is less than the ‘strike price’, the corporate off-taker pays the difference to the renewable generator, and vice versa.

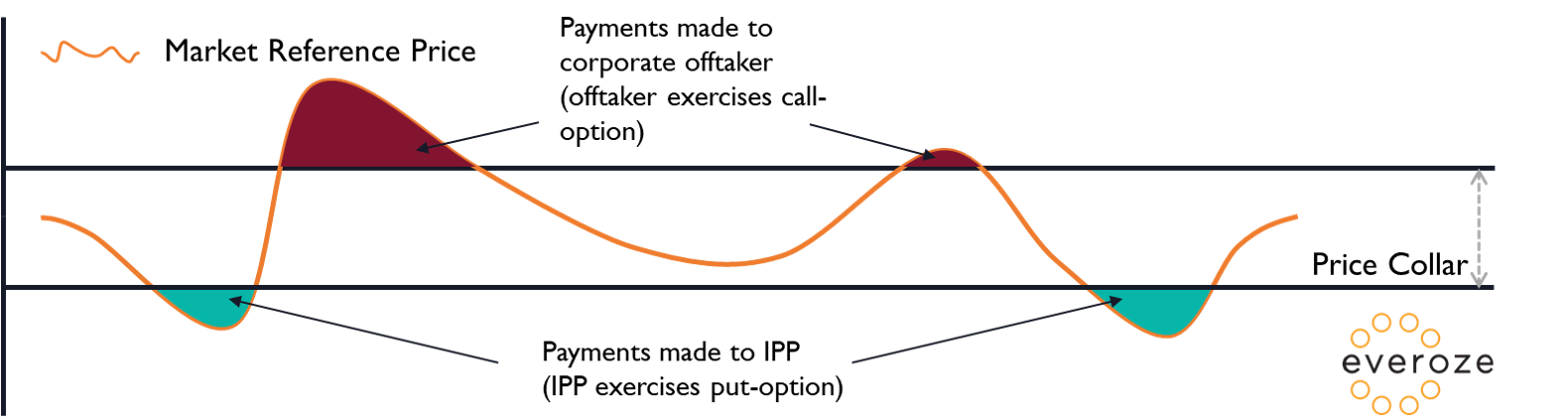

Options or Price Collars

As an alternative to a single strike price, the parties may agree on a floor and ceiling price and grant each other the right to sell-to or purchase-from if the day-ahead market price (or any other reference price) is below or above the respective floor or ceiling price. If the reference price falls below the floor price, the generator exercises its put-option to sell power at the floor price. If the reference price is higher than the floor price, the generator lets the option expire. The inverse applies for call-options where the corporate off-taker is able to exercise its option to purchase power at the ceiling price if the market price exceeds this level, or if the price is below the ceiling price, let the option expire. This mechanism provides a price floor for the generator and cap for the consumer.

It is no surprise then that the strike & collar prices and how these vary over the term of the PPA are the key points of negotiation when it comes to synthetic PPAs.

Besides counterparty risk, which is a key area of focus for developers and investors, and PPA reliability over the term of the agreement, there are other key risks which parties will need to be cognisant of and ensure they are adequately managed. The impact of these risks on the business case must be properly understood – and the best time to do this is at the negotiation stage.

More on the top three synthetic PPA risks in my next post!

In the meantime, if you’ve got any questions /or would like to discuss our experience of key corporate PPA risks, do get in touch.