The upcoming P375 Elexon code reforms will be a game changer for domestic flexibility – Here’s why

Published June 2022

The flex sector has been eagerly waiting for the P375 Elexon code reforms and the accompanying CoP11 metering standard coming into force today. Whilst its a big enabler for utility scale storage co-located with renewables, it is a game changer for domestic flexibility. And it doesn’t end there. There are further reforms in the works to fully unlock flexibility potential in our homes.

The P375 Elexon code reforms together with the new CoP11 metering standard is the next big step for domestic flexibility. And it doesn’t end there. There are further reforms in the works to fully unlock flexibility potential in our homes. Let’s pause, take a moment and indulge in some imagineering with Everoze Partner Nithin Rajavelu.

Imagine a world where you have more than one energy supplier for your home: one for your normal household demand, and a separate supplier for your electric vehicle (EV) charging.

Imagine taking your EV charging tariff with you even when you charge your EV at your office or any public chargepoint away from home.

And imagine getting paid for your neighbour to charge their EV when there is surplus solar from your home, and you aren’t using it to charge your EV or heat your home.

It sounds like science fiction, doesn’t it? Particularly considering our current convoluted system for public EV charging.

What if I told you this may be closer than you think? The Elexon P375 reforms coming into force today is the first of the jigsaw pieces to make this a reality.

What is P375? And why does this matter for domestic flexibility?

Aside from sounding like a beloved character in the Star Wars franchise, P375 is Elexon’s latest code reforms which opens the door for flexibility assets ‘behind the meter’ to participate in the Balancing Mechanism (BM) and provide balancing services.

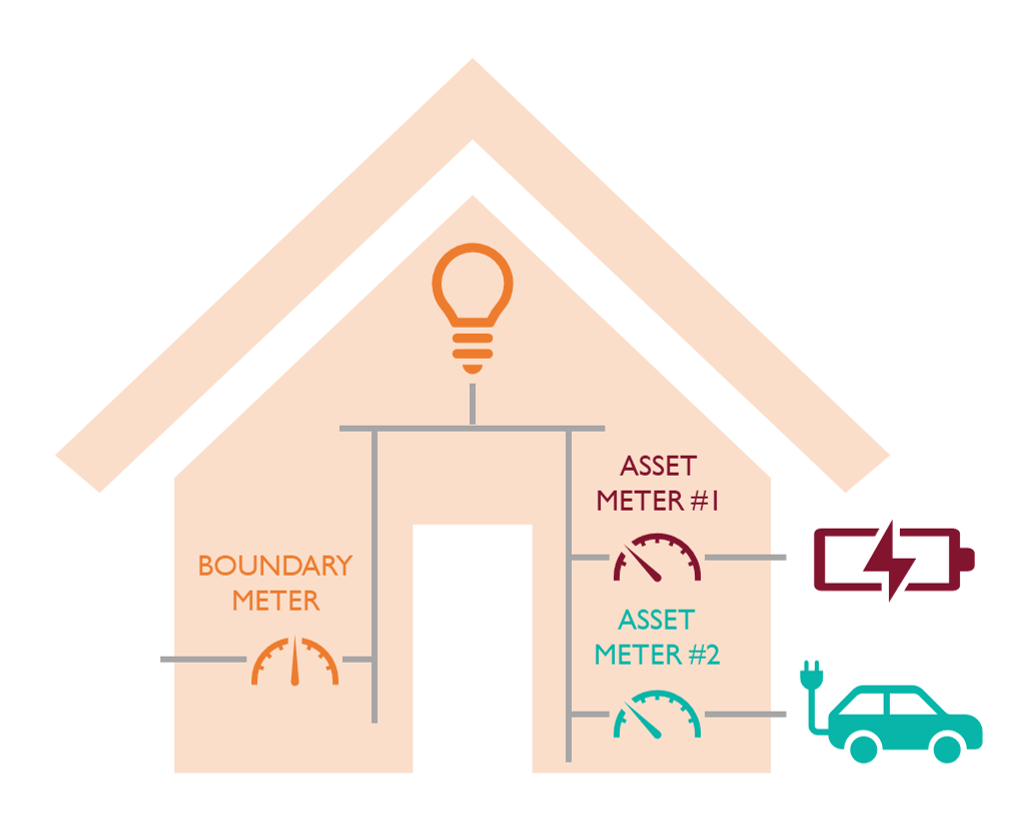

The current rules for participating in the BM require metering to be done at the ‘boundary point’, i.e., the point at which household demand is metered for energy supply. Given the ‘one meter one party’ rule, home batteries and other low carbon flexibility assets in the home can participate in the BM only if the household’s energy supplier is also the flexibility service provider thereby coupling the two roles.

P375 addresses just that, effectively de-linking flexibility service provision from the energy supply function for the household. In a ground-breaking move, P375 introduces the ability to meter flexibility assets behind the meter for the BM. This allows 3rd party aggregators (also known as Virtual Lead Parties) to aggregate flexibility assets like home batteries, EV chargers and heat pumps via Secondary BMUs to participate in the BM without this resulting in any ‘imbalance’ and associated costs to the household’s energy supplier.

It doesn’t end there. The new Code of Practice (CoP) 11 metering standard comes into force alongside P375 setting out requirements for asset-level metering equipment. This new metering standard allows embedded metering in assets to be used for asset-level settlement metering. This reduces overall metering and installation costs for low carbon flexibility assets – a crucial step to increasing deployment and achieve flexibility volumes at scale. Moreover, CoP11 also allows for DC metering to be used. This means, in theory, on-board metering in the EVs can be used for balancing services metering.

Together, these two changes represent a huge step forward for domestic flexibility, opening up access to the lucrative BM as a new revenue stream. But this doesn’t automatically mean batteries and EV chargers up and down the country will be providing balancing services starting tomorrow – far from it. Although National Grid ESO’s dispatch decisions in the BM are based on a price merit order and are technology neutral in principle, there have been instances of flexibility assets like battery storage being skipped despite being in merit (i.e. cheaper than the asset that was dispatched instead). As domestic flexibility assets are new to National Grid ESO, more work is needed to understand how the ESO would dispatch distributed domestic assets and integrate this in their control room operational decisions alongside existing assets with known capability.

What’s next for domestic flexibility?

P375 is a big step forward but there’s more hurdles to cross! The next big milestone in the horizon is the Elexon P415 code reform. In simple terms, P415 enables wholesale energy market trading via Secondary BMUs. With this, flexibility assets in homes can buy and sell energy in the wholesale energy markets without interfering with energy supply to the household.

This would unlock new business models and revenue streams such as (i) trading surplus solar generation in the wholesale energy markets or via peer-to-peer energy markets, and (ii) having multiple suppliers for the household, with a separate EV tariff with a different supplier or aggregator.

P415 is still in its early stages and the proposal is currently being assessed by Elexon. If successful, and that is not a given, it’ll be a good few years before this comes into effect.

Beyond that, more market and regulatory reforms will be needed before you can take your EV tariff with you wherever you charge your EV or sell your surplus generation to your neighbour. It may seem far-fetched now but considering how far we’ve come on battery storage, EV charging and flexibility these last few years I’m betting the industry will continue to innovate and make it happen sooner than you think!