4 GW Spanish solar goldrush ahead – and perhaps a storage boom to follow?

Published August 2017

A huge 3.9 GW of solar projects scooped up contracts in Spain’s big tender. But will investors & lenders get comfortable with the regulatory risk? And can the grid handle it? Everoze Partner and PV veteran Stefan Mau sums up what you need to know.

It’s been a long time coming, but – finally – it looks like the Spanish renewables market has been given a second opportunity. In May and July the Spanish Ministry awarded a total of 3.9 GW contracts to solar projects. This was more than anyone had expected: indeed, bids were so competitive that the initial caps had to be increased.

At Everoze we’re confident that this is an exciting market destined for growth – and are putting our money where our mouth is, having just opened shop in Madrid. Here’s our analysis of the results.

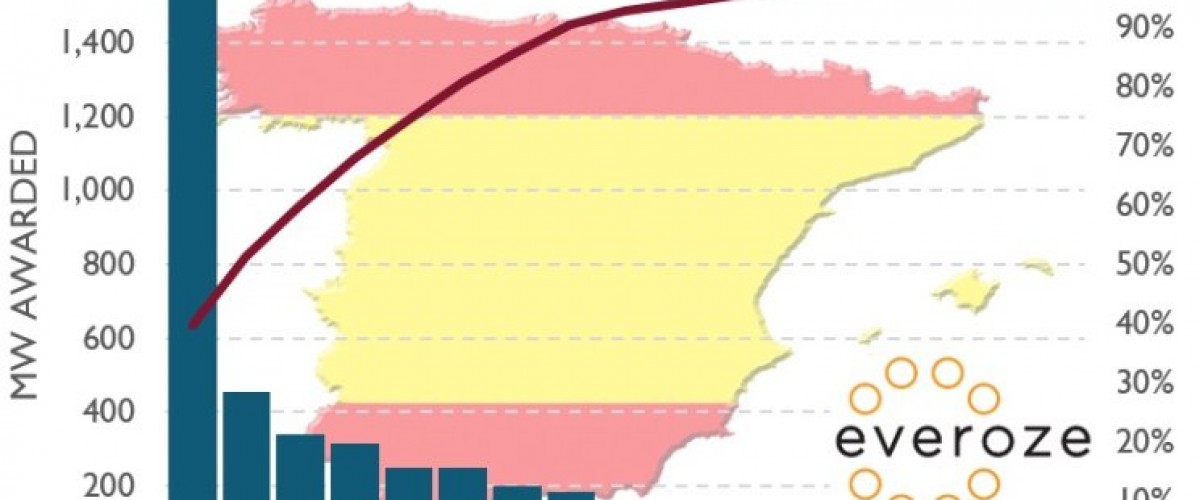

Local players dominate

Congratulations are due to 31 developers who were successful in securing contracts. This included Cobra Concesions SL (1,500 MW) and X-Elio (455 MW), who were together awarded half of the capacity, as shown in the chart below.

Given past experiences with regulatory change, perhaps it’s not surprising that international developers were deterred. This, after all, is a market which has experienced painful retrospective policy changes. As Technical Advisor, we’re also well aware of some of the engineering challenges caused by changing requirements – not least the need for operational projects to implement voltage ride-through changes back in 2010 – leading to costly inverter refits for many.

So, perhaps unsurprisingly it was the local developers who dominated this auction: being closely plugged into the market, they were well placed to assess the residual regulatory risk and the detailed requirements of what constituted a winning bid.

Nonetheless, with almost 4 GW needing finance, there’s no doubt that many will be looking beyond Spain to fund their projects – hunting for forgiving international investors who are prepared to place their trust in the Spanish regime once again.

Good news for consumers

Another striking finding from this auction was that prices came in at 20% below what we see in the market today.

So: how could developers offer this? There are multiple reasons. Most critically, it’s essential to note that the backstop for project development is end-2019, meaning that these are future cost projections rather than current prices. And it’s clear that some players are hoping to squeeze the supply chain through economies of scale – using volume procurement to push down prices. Certainly this is great news for Spanish consumers, who benefit from an influx of energy which is not only green, but competitively-priced too.

Storage boom to follow?

But I’d like to leave you with a final thought. Back in May, wind energy was awarded 4.1 GW of contracts. Adding in the newly awarded solar capacity, this extra 8 GW will take the total capacity of renewables to 59 GW in Spain. This raises the question: what investments in system flexibility might need to follow?

Maybe, just maybe, this forthcoming glorious renewables boom will be followed by a battery boom, as seen in the UK and beyond. That could be yet another reason for international investors to reconsider opportunities within this market. Do you agree? We look forward to reading your comments below!