Anticipating revenue diversification

As published in PV-Magazine 2 November 2020

For all the talk, we must admit there are really very few battery projects on the ground in mainland France. But even in these early days for the sector, writes Bruno Menu, a partner at Everoze, we are seeing an evolution in financial models to more revenue diversification than was anticipated for the first projects. Let’s look at why that is, and what attractive options there may be for revenue diversification.

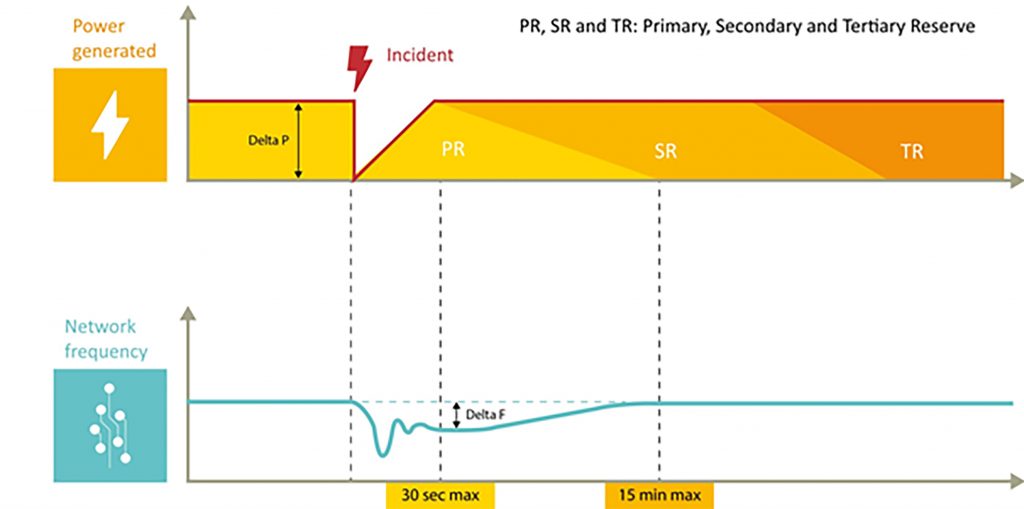

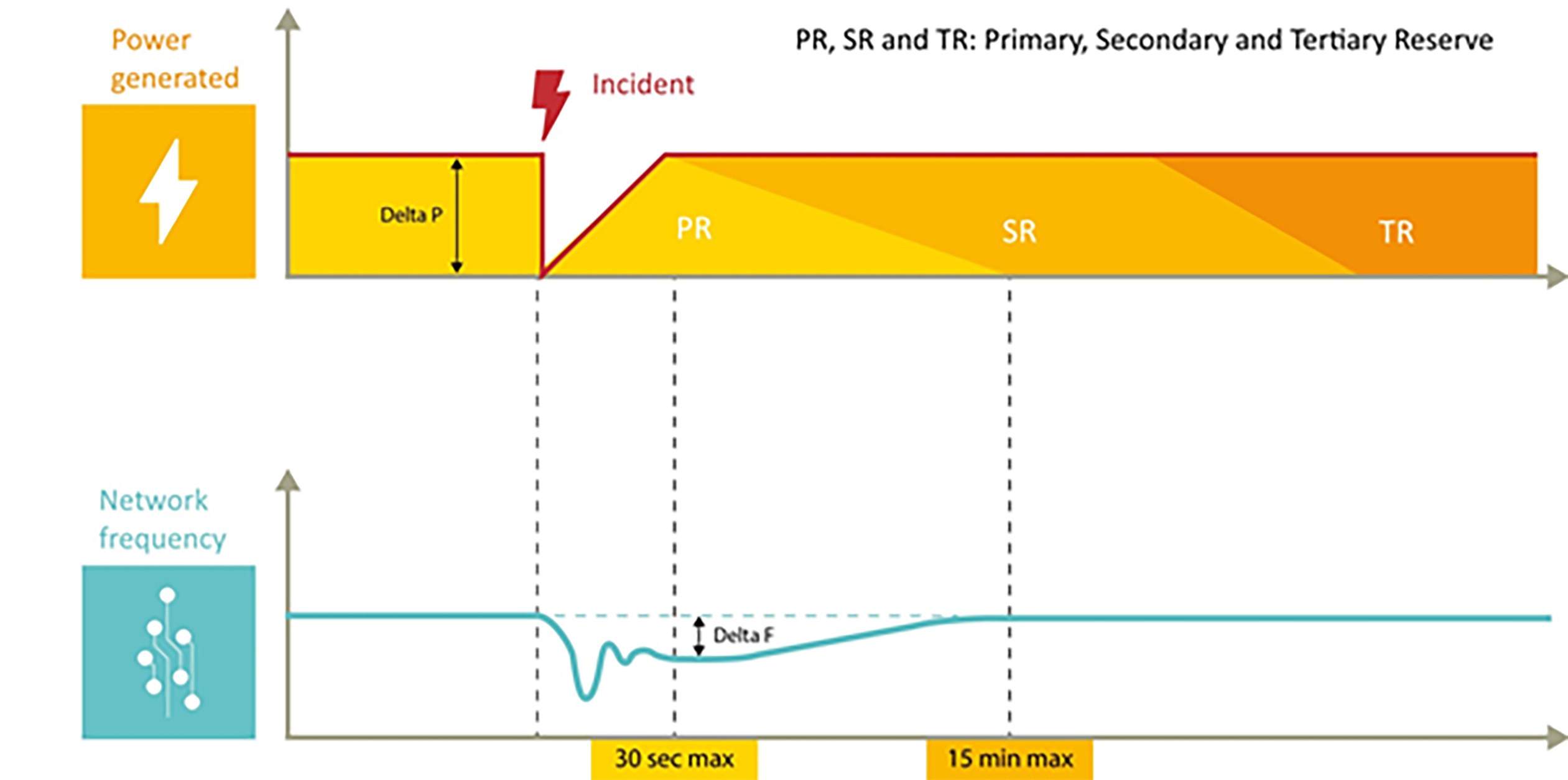

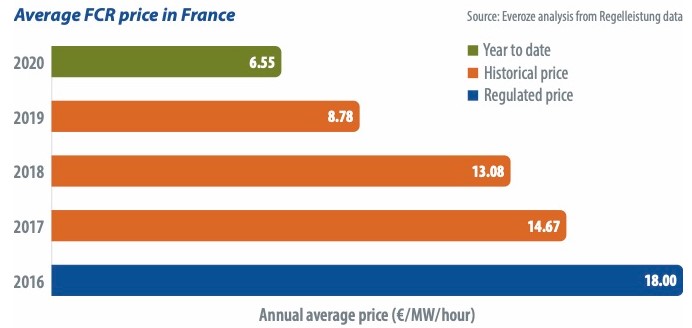

Since the French market opened to battery projects in 2017, revenue from primary reserve – now called frequency containment reserve (FCR) – has been central to the business plans of all front-of-meter battery projects, often combined with participation in the capacity market. FCR is the first line of response for the transmission system to withstand an incident such as the loss of a large power station, swiftly providing active power response proportional to frequency deviations. FCR is remunerated for availability, in €/MW/hour, rather than for activation, with contracts for four-hour service delivery blocks.

Revenue streams

Revenue streams

The opening of the FCR market to battery projects was part of wider liberalization where this service began to be procured on a cross-border European platform. Since this happened, competition between assets and the arrival of new ones such as demand response and batteries has led to a downward trend in the value of FCR. With prices going down, it is less attractive to rely only on this mechanism. Projects need to not only hope for other sources of revenue, but actively plan for them. RTE is planning to liberalize the secondary reserve mechanism by the end of 2021. This market is currently remunerated at a regulated, and very attractive, price of €18/MW/hour. Although the price is expected to decrease with liberalization, the size of the market for secondary reserve is significantly larger than FCR. Batteries by themselves would struggle to get the full value of this service as it requires more energy than providing FCR, but the battery could be used as part of a portfolio to deliver small volumes through an aggregator. Other potential revenue streams include the balancing mechanism and market arbitrage. The balancing mechanism is a close to real time market in which the TSO can pay assets to increase or decrease output to balance consumption and generation at national level. Market arbitrage – i.e. buying (storing) energy at low prices and selling (exporting) at high prices – could be done on day ahead or intraday energy markets. However, our analysis suggests price volatility is currently too low for arbitrage to be viable, especially as this is a more intensive use of the battery and accelerates degradation. However, with more renewables penetration, volatility will likely increase over time and therefore increase revenues.

British example

This type of revenue diversification is already well underway for battery projects in Britain. When the market started to grow in 2016, the revenue stack for batteries was concentrated on primary reserve (FFR) and capacity market. But as more battery projects were built, FFR prices dropped quickly from GBP 20/MW/hour to below GBP 5/MW/hour. There has been a recent upturn in prices, but the market is now saturated and, with more than 1 GW of batteries commissioned, assets are unable to win contracts at a viable level on a long-term basis. Projects are now assuming that they will trade in energy markets and the balancing mechanism for a large proportion of their revenue rather than depending solely on ancillary services and the capacity market.

The challenge of revenue diversity when designing a battery project

FCR, secondary reserve, balancing mechanism and arbitrage all have different requirements, especially regarding the energy capacity of the battery: FCR doesn’t require a large reservoir of energy, whereas revenue from other streams is directly related to the available energy, and sometimes it is not possible to capture a stream without assuring a certain reservoir. So how to size your battery to meet the requirements of multiple markets? There is no easy answer. The first suggestion is to carefully select and work closely with, an aggregator. A battery working alone will not be technically able to access all markets, and optimization is complex. We believe it is optimal for batteries to be pooled with other assets, ideally in a large and diverse portfolio. This is the business of an aggregator. Aggregators have different strategies, so optimal sizing might differ between one and the next. It is important to get their input on sizing to maximize value. Second is to consider, from the beginning, how easy it would be to add capacity to your project. This will benefit from expected price drops for battery cells. But if not considered in the initial design, it can be disproportionally expensive to add capacity in the future.