UK Capacity Market: 4.7GW batteries have prequalified for T-4 but can creative sector bounce back from de-rating debacle?

Published December 2017

The UK’s Capacity Market (CM) Prequalification Registers and De-rating Consultation Response are finally out – and contain a few surprises for the battery storage industry. In this blog, we summarise Everoze’s takeaways from these two landmark publications.

A sizable, shovel-ready pipeline is here

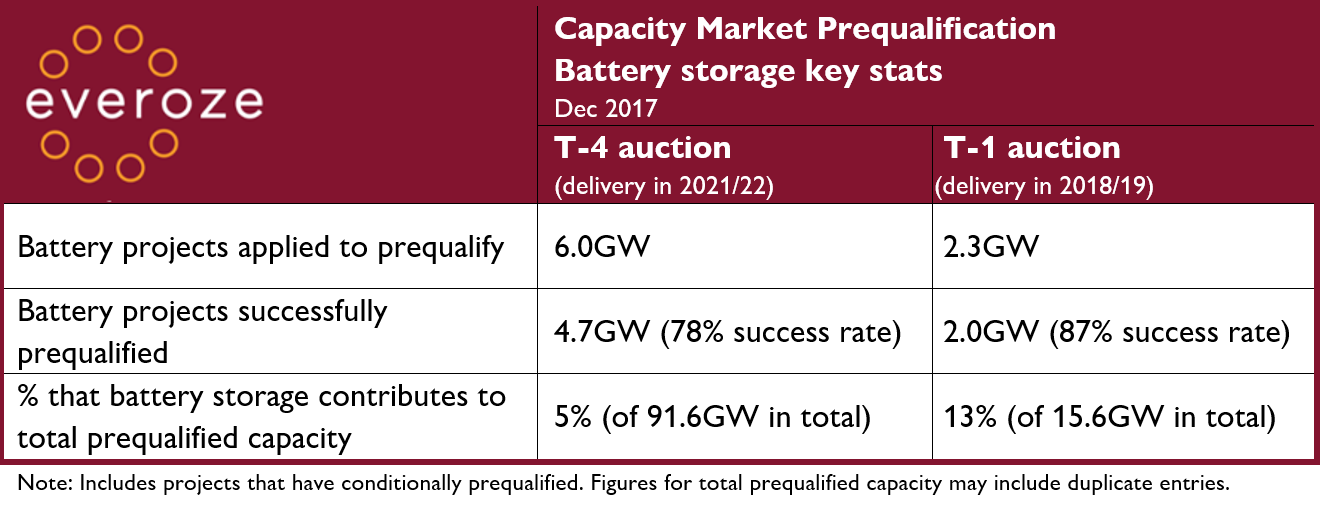

The data shows that the sector has certainly moved on from the last auction, with a whopping 4.7GW battery projects successfully prequalifying for T-4, all bar two targeting 15-year contracts – key stats are in the table below. For reference, in the CM T-4 auction last year 1.5GW of batteries sought to prequalify.

Meanwhile, 2GW of batteries prequalified for the T-1, signifying a vast near-termpipeline. The T-1 auction kicks off on 30th January and successful projects will need to be operational by 1st October 2018. This frantic project activity aligns with our own anecdotal experience: a year ago the Everoze team were busy with feasibility assessments, and early procurement/ contractual support; this year, we’re already dusting off our boots from site visits for the first operational large-scale projects.

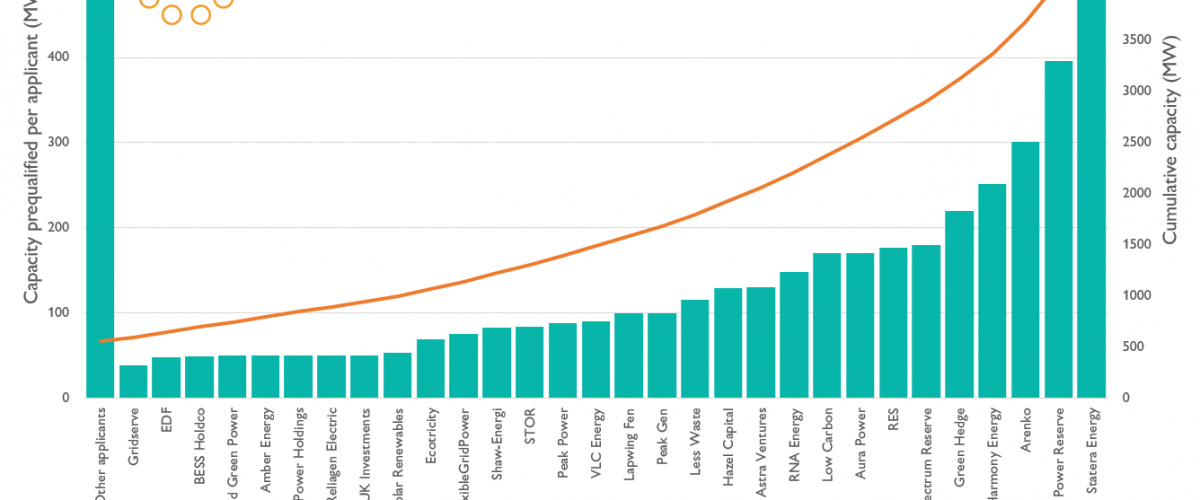

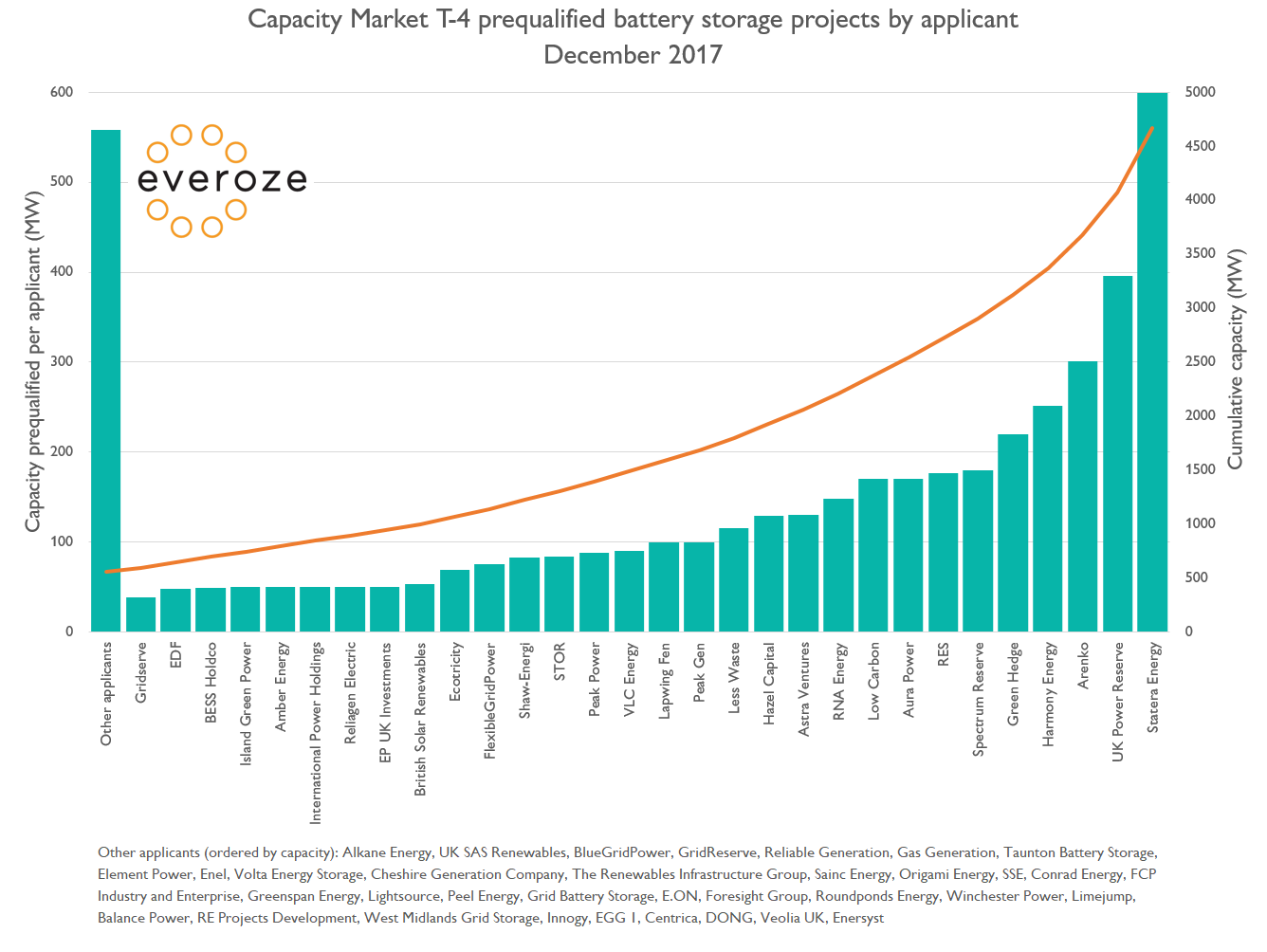

But where it gets really interesting is seeing who has prequalified, depicted below. We need to add the usual caveats here – this has involved a few inferences, some SPV-detective work and removal of obvious double-entries (let me know if you feel we have misrepresented your company – we’ll happily update).

Some key takeaways emerge:

- 65 companies successful: so many secured prequalification, in fact, that our chart only shows the top 30 because there simply wasn’t enough space to show them all.

- Big utilities barely visible: A number of major utilities have bid in some capacity – but the striking thing is that 98% of capacity is coming from other more entrepreneurial players – particularly developers from renewables and peaking plant backgrounds. Unlike the big utilities, these third parties often can’t finance projects on balance sheet – creating opportunities for equity investment.

- Behind-the-meter is continuing in the background: Finally, we want to clarify that this chart only shows part of the storage deployment story – focused largely on front-of-meter utility-scale projects. Meanwhile, there’s a bubbling market in behind-the-meter storage co-located with energy users that isn’t clearly visible, partly because some parties may be selecting alternative CMU classification.

Storage de-rating is a blow

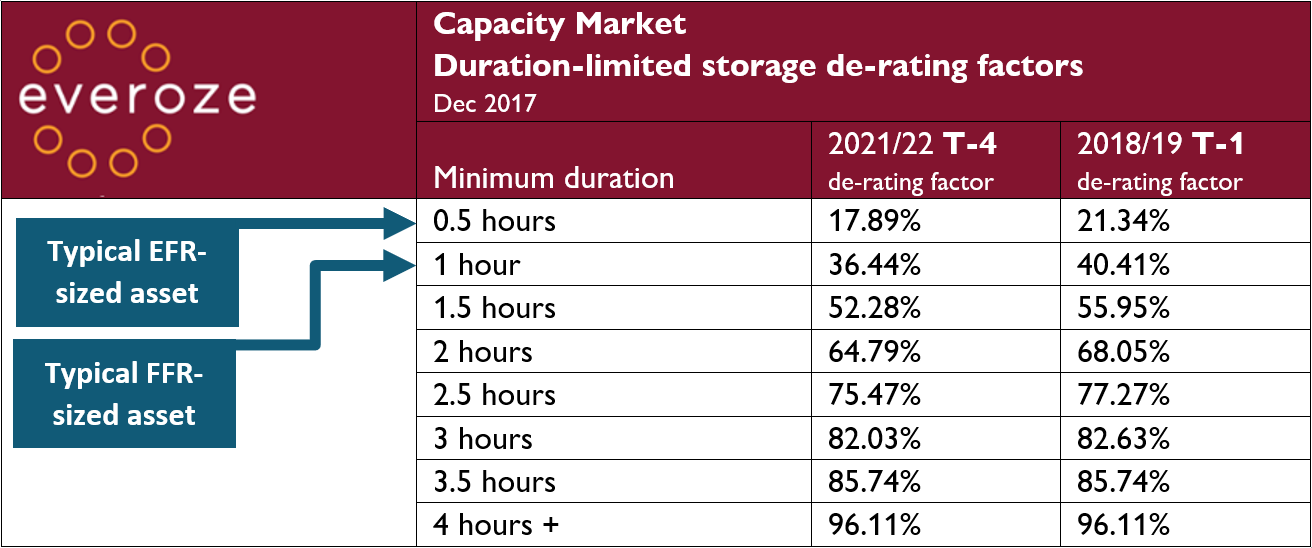

The second big announcement is on CM storage de-rating factors. Simply put, de-rating factors reduce payments to storage projects in an attempt to reflect their contribution to security of supply. BEIS has now confirmed that batteries will face big de-rating cuts to reflect the limited duration of support they offer.

These are huge changes. As an example, FFR-style batteries see their revenue cut from the baseline of 96% to 36% of the clearing price in the CM T-4 auctions. See the table below.

Followers of Everoze already know our views on this: we believe these de-rating changes had an inevitable logic but were highly critical of the tone and timing of their introduction. They come as a blow to an industry already reeling from concerns about market saturation in the frequency response market, following the publication of National Grid’s FFR Market Information report for December.

Don’t underestimate the sector

In this uncertain context, there have been early reports of a battery bloodbath, with projections of substantial drop-outs amongst the 4.7GW of prequalified batteries when bidding into auctions in the New Year. The drop-out risk is particularly pertinent given how many of the leading auction participants are dependent on securing third party finance. For reference, last year we saw an attrition rate of 2/3.

But Everoze’s view is clear: our electricity system is fundamentally changing. Energy storage is and will continue to be a key enabler in this transformation. For many, the ‘learning by doing’ that comes from investing in flexibility technologies is a strategic imperative, not some optional punt. Moreover, we’re already seeing diversification away from ‘vanilla’ revenue stacks of frequency response and CM – with movement towards exploiting merchant revenue opportunities, unlocking digital inertia potential, and/or positioning behind-the-meter. Longer-term DSO revenues are also growing in importance.

So yes, these CM de-rating announcements are challenging, even painful, and will most likely kill off some projects. But the drop-out rate may be lower than you suspect. Our advice, as ever, is not to underestimate the sheer grit and creativity of our emerging storage industry. The wider strategic logic for storage remains unchanged.