A contrarian’s viewpoint on REMA & GB wholesale market reforms

Published October 2023

A contrarian’s viewpoint on REMA & GB wholesale market reforms (plus a 2-min briefer on locational pricing)

We agree with Everoze Partner Nithin Rajavelu – It is a strange yet exciting time to be working in the energy sector. In this fascinating blog, he outlines his four contrarian viewpoints with adopting a locational marginal pricing (LMP) model for GB.

It’s been a year since BEIS (now DESNZ) kicked off the Review of Energy Market Arrangements (REMA) consultation on what the future of our electricity market framework should look like, including fundamental changes to how the wholesale energy markets would function. A big part of this consultation is on introducing locational wholesale energy pricing which will have a big impact on current and planned renewable generation and battery storage projects. In this blog we explore what all of this may mean for renewables developers and asset owners if implemented.

It is a strange yet exciting time to be working in the energy sector, wouldn’t you agree?

We have set ourselves an ambitious target of decarbonising our electricity system by 2035. The market mechanisms and the grid infrastructure aren’t there yet to fully support the scale of new low carbon generation needed for a zero-carbon electricity grid.

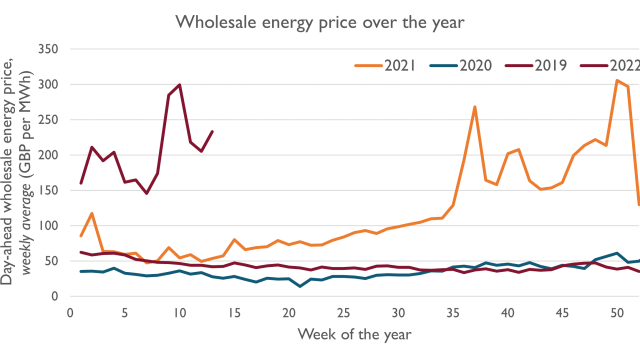

At the same time, energy prices have been at an all-time high for the last couple of years, primarily driven by global gas prices, which together with the climate driver makes a strong case to wean our dependence on fossil fuel fired generation.

How do we make the changes needed to deliver on our net zero targets whilst keeping consumer energy bills low?

BEIS made a compelling case for market redesign in their Review of Energy Market Arrangements (REMA) highlighting the need to provide efficient locational price signals to create the conditions needed to support a high-renewables electricity grid while minimising costs to the consumer. National Grid has made a similar argument in their Net Zero Market Reform (NZMR) programme (more in their Phase 4 webinar) where they forecast huge increase in constraint and balancing costs up to 2030 under business-as-usual, with current market signals for storage and interconnectors exacerbating constraints and increasing cost to the consumer.

The case for change is indubitably clear as further demonstrated by the work done by the ES Catapult. While I don’t dispute the underlying principles and the theoretical benefits to the consumer from adopting locational pricing for our wholesale energy markets, I am conscious of the clash with the realities of the GB renewables sector and what this means for current and planned renewable generation. If you are not familiar with locational nodal and zonal pricing concepts, see the two-minute briefer included further below.

At the risk of being unpopular, here are my four contrarian viewpoints with adopting a locational marginal pricing (LMP) model for GB:

(1) Scottish onshore and offshore wind will be materially impacted under an LMP model. While I understand the ‘systems approach’ taken under REMA, the realities of the GB electricity sector is that we have c.10 GW of onshore and offshore wind capacity installed and connected to Scottish grid, and many more GWs in the pipeline, particularly offshore wind (cue ScotWind). I am conscious under a zonal or nodal price model this risks severely depressing wholesale energy prices for Scottish wind impacting both operational and planned projects. While projects with CfD contracts may not be affected as much (if grandfathered under the new framework), that cannot be said of the GWs of onshore and offshore wind projects not under CfD and looking to go the PPA route or even go ‘merchant’. The same can be said of solar PV in southern England to some extent, where we might start seeing the ‘duck curve effect’ in the wholesale prices in zones or nodes with lots of solar generation already connected to the network.

(2) There is a considerable risk of impacting investor confidence without widely accessible price stabilisation mechanisms. Granted, LMP models are successfully used in other markets like Texas and the Nordics. However, in contrast to when the new nodal or zonal market design was introduced in those markets, there is already a huge volume of installed renewables capacity in Scotland and many more GWs contracted under lease and CfD. If the wholesale market reforms are not coupled with some form of price stabilisation mechanism (like the CfD albeit an improved version), the impact on Scottish onshore and offshore wind in particular as described above, I fear will impact investor confidence and risks increasing cost of capital and/or slowing down renewables deployment until there is clarity on the future market design, and overall jeopardise achieving our 2035 decarbonisation targets.

(3) LMP weakens the incentive for the system operator to proactively plan additional transmission capacity. Under a locational pricing model, generators and consumers bear the full responsibility for locating in areas where there are no network constraints, and bear the financial impact for not doing so. In essence, this pushes the primary responsibility for resolving system constraints onto the “market” along with the financial consequence for not doing so. While I don’t disagree that efficient siting of generation to avoid large pay-out of constraint payments at the consumer’s expense should be avoided, I would stress that this should come hand-in-hand with proactive and strategic network planning. We need big, bold and urgent build-out of strategic transmission capacity as put forward in the Electricity Networks Commissioner’s report which argues for a Strategic Spatial Energy Plan and to avoid network upgrades lagging behind generation capacity build-out ambitions.

(4) On a positive note, LMP strengthens the case for storage and flexibility. Energy storage and flexibility can certainly help stabilise the price volatility in constrained zones and nodes. So project developers and asset owners will need to start thinking about co-locating battery storage alongside their renewables assets, or at least the optionality of retrofitting at a later date, to future-proof their investments. National Grid ESO in their 2023 Future Energy Scenarios has forecasted 47 GW of storage and flexibility being needed by 2050 which is positive news for this industry driving big investments, particularly in Scotland with high penetration of wind generation behind the England-Scotland constraint boundary. Demand side flexibility (DSF) and energy efficiency however seem to be missing from REMA. While these technologies are not big needle swingers, DSF in particular has demonstrated to be a key part of National Grid ESO’s flexibility toolkit for constraint management. Perhaps they will be part of the retail market reforms Ofgem has kicked off with a Call for Evidence in July this year.

Is this worth the price?

To reiterate, I fully agree with the underlying thesis for change – business as usual is not going to create the conditions needed to get to net zero. We need bold changes to achieve decarbonisation.

My cautious scepticism is more with what fundamental changes like nodal or zonal pricing would mean for the GB renewables sector which has grown and taken shape over the last few decades under a very different policy and market landscape. While a particular set of solutions have shown to work in a different market with different conditions, does not necessarily mean it would hold true for the GB market also.

Maybe I’ll look back and realise my concerns were unfounded after all – I’d be glad to be proven wrong as long as we can collectively achieve a net zero energy future!

I’d be eager to hear what you think locational pricing and the other package of reforms in the works mean for GB renewables and flexibility.

—

Two-minute briefer: what is locational pricing and how is the price set?

Our current GB wholesale market is based on a national pricing model, where all generators and suppliers receive a single national wholesale energy price irrespective of their physical location. Locational pricing, as the name suggests, provides a different wholesale energy price for each geographical/network location depending on the local generation and demand levels, and network constraints. The REMA considers two models under locational pricing – zonal and nodal pricing.

Under zonal pricing, the country is divided into a number of zones (c.5-10 zones) reflecting transmission network boundaries. Each zone will have a different wholesale energy price for all generation and demand within the zone. Example, the Nordic electricity market uses a zonal pricing model.

Nodal pricing is zonal pricing on steroids where the country is divided into several nodes (c.50-100 nodes) each representing a location in the transmission network. Similar to the above, each node will have a different whole energy price. Example, the Texas ERCOT market uses a nodal pricing model.

The wholesale energy price in each zone or node is set by the balance of demand and generation in that zone/node as well as transmission network constraints influencing that zone/node. It’s far more complex than this but this is the simplified version. In simple terms:

- If generation is greater than demand in a zone/node, and there are transmission constraints to evacuate this generation to zones/nodes which have higher demand than generation, then the price in this zone/node will be lower than the national average. The price will be depressed further if the constraints are higher relative to the surplus generation in that zone/node.

- And vice versa, if demand is greater than generation in a zone/node, and there are transmission constraints to import generation from neighbouring zones/nodes, this will have an upward pressure on prices in this zone/node and the price will be higher than the national average. As above, the higher the constraints to import generation into that zone/node, the higher the price in that zone/node.