Time for batteries to scalar up on the Island of Ireland

Published September 2017

Everoze Partner, Paul Reynolds sees an opportunity for batteries under the DS3 reforms of system services on the Island of Ireland. Here are his key takeaways – how the system works, and what a winning revenue strategy looks like.

Ireland is great.

Obviously there are the people (especially my Irish wife!), but less well known, is that the Island of Ireland is a world leader when it comes to integrating renewable energy into the grid.

Over the past decade the island has embarked on radical reforms to deliver a power system that can operate with a penetration of 75% of non-synchronous generation (wind, HVDC interconnectors and solar) at any one time. This metric is called SNSP – system non-synchronous penetration level. A key step in achieving 75% is finalising the procurement approach for system (or ancillary) services, with major reforms recently consulted on.

The result: a positive outlook for batteries. Let me explain…

System Services

There are 14 system services proposed in Ireland shown below.

For batteries the focus is likely to be on Fast Frequency Response (FFR), Primary Operating Reserve (POR), Second Operating Reserve (SOR) and Tertiary Operating Reserve (TOR1 & TOR2).

Although the plan is to eventually to move to competitive tendering, services are procured through a panel based procurement process whereby if providers can demonstrate technical compliance they are added to the panel. Providers are then paid when available according to the following formula.

Tariffs are set by the system operators Eirgrid and SONI, with the base tariff for FFR quite low. The volume is based on availability to provide the service (as opposed to utilised) and is calculated in MWh.

Scalars

The interesting part are the scalars. These give the system operators (SO)s flexibility to incentivise good behaviour or penalise bad behaviour, with different scalars applying to different revenue streams.

If we focus on FFR, the most significant scalar is the scarcity scalar which is for FFR zero up to an SNSP level of 60%. 6.2 between 60-70% and 8.5 when the SNSP is above 70%. In other words, FFR is paid well at high penetrations of wind/interconnectors; but only paid at high penetrations. As we will see this makes a big impact on revenue uncertainty.

A range of other scalars then seek to drive:

- Robust performance, with payments reduced substantially for any non-delivery;

- A fast response, with a scalar of 3 if a response is provided within (a very fast) 0.15 seconds (in time to deliver RoCoF reduction benefits);

- A dynamic response, with a scalar of 1 if a dynamic response is provided to a frequency sensitivity of +/- 0.015Hz (equivalent to the UK’s Enhanced Frequency Response Service 2 specification); and,

- A longer duration response, with a scalar of 1.5 if the battery provides FFR, POR, SOR and TOR1.

All this means that, assuming no performance issues, a battery could earn ~28x the base tariff at periods of 60-70% SNSP and ~38x for SNSP levels above 70%.

SNSP levels

But there’s a challenge. The time spent above this SNSP level will vary significantly from year to year. This is because SNSP level is a function of the generation mix, wind speeds, interconnector flows and demand levels in a given year.

The table below shows system operator estimates for 2019/20 under two generation mix scenarios. As can be seen in a bad year you could be above 60% SNSP for 7.8% of the year. In a good year you are up at 29%. This is a huge variation, completely out of the control of battery developers.

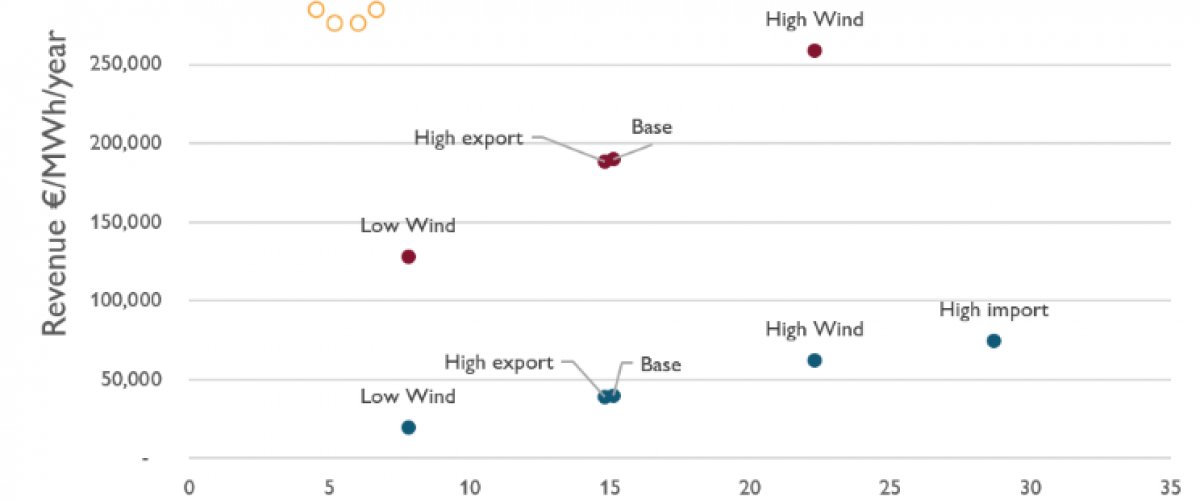

Revenue estimates

Putting all this together and with the SNSP limit increased to 75% and the ‘New providers’ generation mix, at Everoze we estimate that for a battery with no performance issues, a dynamic response within 0.5 seconds to a 0.02Hz deviation in frequency (up or down) and provision of FFR, POR, SOR, TOR1& TOR2 (20 min duration in total) then revenue could be ~ €300k in a good year and ~€128k in a bad year.** This excludes consideration of other revenue streams which might be stacked in with this (e.g. payments under the Capacity Renumeration Mechanism).

Chart: Maximum annual battery project revenue under different SNSP levels.

So what?

Having worked as Technical Advisor to investors and developers for a number of GB battery projects, Everoze notes three striking implications of DS3 design for batteries:

1. Revenues are attractive but variable: The base case revenues are likely sufficient to drive new investment, but investors will need to get comfortable with inter-annual variation and the level of regulatory certainty.

2. A probability-based approach is essential: In much the same way that we see wind projects use probability distributions to account for wind variability (with P50 and P90), battery storage projects will need to use probability distributions to account for the differences in revenue from year to year, albeit that SNSP is unlikely to have a normal distribution.

3. Wind forecasting will help: Wind forecasting will likely become a key input into battery control systems, with battery developers needing their systems to guarantee availability whenever wind speeds are high.

As ever, we would love to hear your views and comments. As I am now on parental leave, if you would like to discuss further please get in touch with Felicity Jones (felicity.jones@everoze.com).

Notes:

*Graph shows time spent above 60% SNSP as a proxy for time above 70% SNSP. The underpinning calculation considers time above 70% SNSP.

**All figures are subject to confirmation in final scalar design.