How the offshore wind market has exploded

Published 13th October 2020

In his latest blog, Everoze Partner Graeme Wilson explains what offshore wind has in common with toilet rolls.

Strange as it seems, pasta, flour and loo roll all serve as useful analogies for what many investors are currently experiencing in their attempts to secure equity an offshore wind farm.

Incumbent offshore wind project investors, who had until recently occupied the majority of the space in the offshore wind equity market, are facing the same frustration as many of us did earlier this year when visiting our local shop, hoping to buy a some loo roll and a bag penne pasta, only to find the shelves bare.

We at Everoze are seeing the offshore wind market place exploding with new entrants. At this point we’re not sure whether panic buying has set in yet, but what is for sure is that demand for an equity stake in an offshore wind project has never been so high.

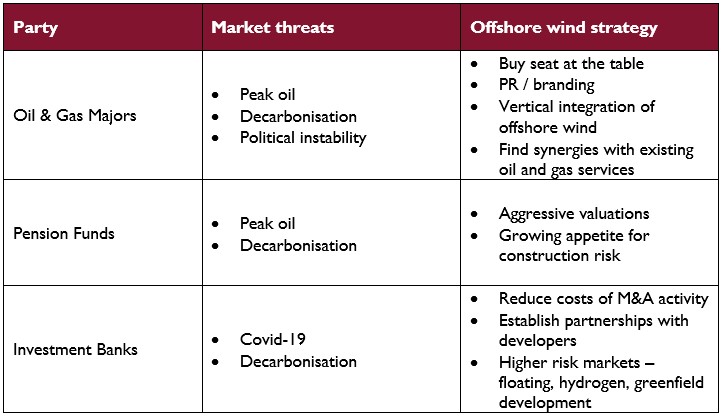

This change is making us re-think how we best serve our clients and causing us to question where the industry is heading. To understand this, we should look at the three main players in offshore wind equity investment.

Oil & Gas majors make their entrance

Offshore wind provides many oil and gas majors with a potential safe haven: it’s somewhere they can invest lots of cash that would otherwise be tied up in fossil fuel assets which are quickly turning into liabilities; there are attractive subsidy regimes; an ambitious development pipeline; and there are also potential synergies with floating wind and hydrogen.

In March 2020, as the pandemic caused oil and gas importers across Europe to lockdown, and as the Russia-Saudi Arabia oil price raged, many oil & gas majors found themselves horribly exposed. As well as the emergence of Covid-19, there had until that point been a long term reduction in demand due in part to the success of renewables.

Many oil & gas majors had already seen that the writing was on the wall before Covid-19 struck. In 2019, Repsol cut the value of their oil & gas assets by $5 due to the weakening outlook for oil and gas prices due to the global transition to a lower carbon economy. While BP included a $2.6 bn impairment charge in their 2019 annual report due to weaker oil prices.

In June 2020, as Covid-19 and the oil crisis raged, Total made their acquisition of 51% of Seagreen. While more recently in September, BP has announced its formed a strategic partnership with Equinor in the US. Both companies bought into these ventures aggressively and its likely other oil & gas majors will soon do the same on other projects elsewhere.

To understand their aggressive valuations it is important to note that these offshore wind projects don’t have to realise their ambitious valuations for the business case to make sense; buying into an offshore wind project provides other benefits to oil and gas majors.

Firstly, it allows them a seat (of which there are few) at the table. This allows them to gain valuable knowledge of the industry from which they could start acquiring the supply chain and attempt to vertically integrate their company. Offshore wind equity also provides them with an opportunity to re-brand themselves as a green company. These additional benefits allow them to be so aggressive with their valuations.

Pressure on pension funds to decarbonise

Another driver for oil and gas majors is the increasing public pressure to decarbonise. Extinction Rebellion and others are making the public more aware each day how the fossil fuel system has pervaded the financial system and our economies.

But its not just oil & gas majors who are aggressively buying up projects for this reason. Pension funds have also come under pressure to decarbonise their portfolios.

To decarbonise their funds and invest in offshore wind, pension funds must however fight with the new entrants from oil & gas as well as the incumbents. One way they could do this is to show an increased appetite for risk and invest in projects at FID, therefore taking on construction risk. Another is to take advantage of their low hurdle rates and aggressively drive up project valuations, out of reach of the investment banks.

The pressure to take this risk was highlighted in recent high profile cases involving the Church of England and MP Pension Funds (worth a combined total £3.5 bn). It is clear that pension funds must consider the environmental and social costs of their investments. These are many other funds under similar pressure to reinvest away from fossil fuels to meet these aims.

With all this pressure to invest, it is important however to consider the size of the offshore equity market – in 2019 the total project acquisitions in offshore wind was €7.4 bn. The available equity is therefore very small compared to the size of funds and the nature of the transactions mean the risk of losing out completely is relatively high.

Investment banks toiling in Covid-19

Many of those incumbent investment banks who were already feeling the pressure to decarbonise, are now pursuing offshore wind investments even more aggressively. Covid-19 has had a direct impact on many of the other markets they regularly invest in.

From March, those who can have been working from home no longer commuting to our city offices and many of us have cancelled flights, rendering the airports empty. Many firms are questioning the long-term value of commercial property and some speculate that working from home could become the norm for many of us in the post-covid future.

Offshore wind investments form part of many investment bank’s real asset portfolios. As well as power and energy – of which offshore wind features alongside fossil fuel investments and other renewables – real assets also include real estate and infrastructure. Real Estate investments include office space, retail such as large shopping centres, student accommodation and hotels. Infrastructure investments include airports, toll roads and motor way service stations.

For obvious reasons, the Covid-19 pandemic and the many resultant lockdowns has hit many of these investments severely. For many of the incumbent offshore wind investment banks, offshore wind has probably never been so attractive.

Conclusion

There has been a shift in the offshore wind equity market. What was once a relatively small group of investment banks and developers, has grown very quickly to include international oil & gas majors and pension funds. Each party is pursuing a different strategy to overcome similar market threats.

Many new entrants from oil and gas may be happy to accept ambitious vendor technical assumptions because they have an underlying strategic reason for investing in projects. Some investment banks are already looking to invest in projects further up the value chain and may start to become more passive when it comes to new M&A opportunities for operational projects because they are struggling to compete with pension funds.

Much like many of us were forced to experiment with courgette spaghetti in March, these investors are all adapting to the changing market.

At Everoze we too are adapting. We remain confident there will be always be demand for quality technical due diligence and access to valuable knowledge and insight, but we are going to begin adapting our approach in the coming months to allow us to better serve our clients in light of these recent changes in the market.

This competitive market means that due diligence needs to be carried out in a more targeted and concise manner and that the approach will need to be adapted on a client-by-client basis.