Spanish wind and solar market: latest round-up

Published November 2017

Spain’s big renewables conference was certainly lively this year. Here are Everoze’s takeaways for those who missed it.

Hats off to APPA Renovables for organising an excellent renewables conference in Madrid last week. It was certainly energetic: with 8GW of wind and solar projects awarded contracts this summer, industry has been kicked into action once again – as summarised in Stefan Mau’s blog post.

Now we’ve had time to digest everything that was said, here are Everoze’s top three takeaways for investors, lenders and industry players eyeing up the investment opportunity…

1. Financiers are concerned about the pool price, debt sizing and wind measurement risk

Although financiers of existing Spanish projects are understandably preoccupied by the regulatory risk of the IRR-setting regime, for financiers of new projects, the concerns are a little different. These were the recurring themes at conference:

- Projecting the pool price: There is pervasive concern regarding pool price forecasts, given historical experience of price projections differing substantially from out-turn prices – a problem that’s been seen across Europe. This is driving lenders’ conservativism in modelling flat and low pool price scenarios.

- Debt consensus: The market consensus seems to be settling at debt terms of 15-16 years in wind and 17-18 years for PV after Commercial Operations Date.

- Risk in wind energy yield studies: Spain faces a particular challenge in wind energy yield assessments. Due to the recent hiatus in project development, installed met masts are typically substantially shorter than the hub heights of the latest turbine models, which causes analytical challenges in projecting energy yield – though my colleagues Bob Hodgetts and Richard Whiting reassure me that there are technical solutions here.

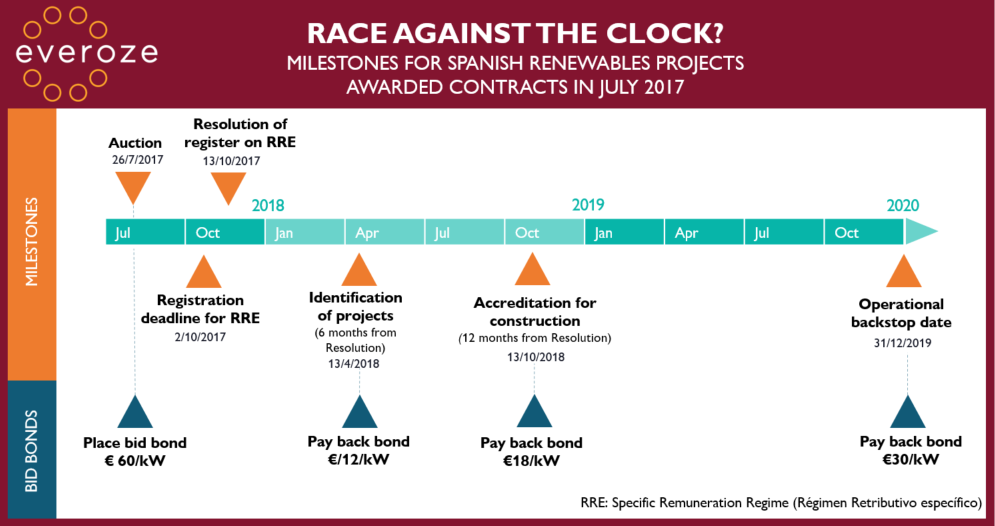

2. Timelines for 8GW of projects are looking tight – especially for wind

8GW projects are all rushing to meet the same deadline: 1 January 2020. For solar this should be achievable, though we still expect a scramble of activity in 2019. For wind, the challenge is even harder due to greater logistical challenges – such as securing a sufficient number of cranes.

Overall, Everoze’s assessment is that the timelines will be tough for some but definitely achievable – see our Gantt chart with key milestones below, based on the July 2017 auction.

3. System issues are a long-term challenge

The third and final theme at conference was system issues. Specifically:

- The mismatch of generation and demand: Since 2005, generation in Spain has grown by 40% whilst demand has remained stable – and it is not expected to increase significantly. This issue is exacerbated by limited interconnection capacity – sparking discussions of investing not only in interconnection with France, but also potentially with the UK.

- Unclear plans for existing generation: As a renewables pioneer, Spain now has a number of ageing wind and solar farms, meaning that planning for actions such as repowering is gaining in urgency (see Everoze’s Life Extension Assessment Framework for details). Similarly, the plans for retiring old coal and nuclear plants are unclear.

- European market interface: From around Q2 2018 Spain will start to participate in an integrated daily market – changing the commercial context in which projects operate.

Your thoughts?

These were just some of our takeaways, based on our role as Technical Adviser – but what are your thoughts on the Spanish market?