What the UK’s landmark storage tender means for France

Published September 2016

The UK’s shock results from its 200MW tender show that battery storage for frequency response is cheaper than any other technology. We summarise what this means for France.

Friday 26th was a dramatic day for energy storage. It was Results Day for the UK’s 200MW storage-friendly tender for Enhanced Frequency Response (EFR).

The tender for four-year EFR contracts was run by National Grid, the UK equivalent of RTE. National Grid introduced this tender to help it keep system frequency within normal operating limits, which is becoming increasingly challenging given the changing energy mix. EFR providers had to offer a solution which could kick in within 1 second, and provide a service for up to 15 minutes at a time.

The competition was fierce: 37 bidders were fighting for contracts, submitting bids for 64 sites. Although the vast majority of bidders were for storage, demand side response providers and one coal plant also bid. It certainly kept my Everoze colleagues in the UK busy, providing commercial and technical support to bidders.

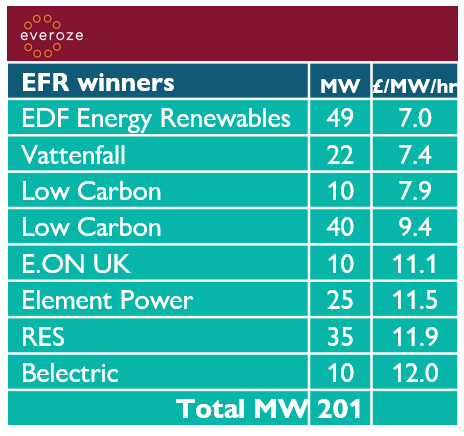

In the end batteries won out: 8 contracts were awarded, the largest of which was a 50MW project by EDF. But perhaps most surprising was the prices. Winning bids came in extraordinarily low at £7-12/MW/hr. This in part reflects the hunger of bidders to gain early mover advantage – but it also shows that batteries are very cheap. National Grid says that this tender will save them £200mn over the next 4 years, compared with the cost of alternative ways to provide frequency response.

3 things this means for France:

For those not familiar with Primary Response in France, RTE is currently obtaining some 570 MW of Primary Response from 10 reserve providers, which include the main generators in France (their participation is compulsory) and a few demand response aggregators. RTE is likely to join in the Frequency Containment Reserve (FCR), a cross-border collaboration (with TSOs from Germany, the Netherlands, Switzerland and Austria) in 2017. The FCR TSOs obtains Primary Reserve through a joint weekly tender and allows for some Primary Reserve to be imported / exported.

So what does the EFR results mean for France?

Most obviously, it’s striking that a French company (EDF), albeit a major participant in the UK power sector, won the largest contract. However, at Everoze we think there are wider implications here:

- Storage can deliver significant savings on frequency control procurement: . RTE is currently procuring Primary Response at 18 €/MW/h. Average prices in the Frequency Containment Reserve have ranged between 12 and 30 €/MW/h in the past year. The EFR tender has come out at the lower end of this range, while providing significantly more value due to the quicker response times. The cost-effectiveness of batteries to provide super-fast frequency response cannot be ignored.

- Long contracts help spur investment: At present the FCR TSO’s procures Primary Reserve on a weekly basis. This is in stark contrast to EFR which offered 4 year contracts. Longer contracts reduce risk, making the projects far more attractive and contributing to the lower costs achieved in the tender. In Germany, STEAG just commissioned a pilot 15MW Li-ion battery system to provide Primary Reserve through FCR and has plan to build another 5 identical units. While other investments in battery may occur under FCR’s weekly tender regime, on the back of EFR, it is likely that TSOs in FCR will wish to accelerate their deployment and reduce the cost of Primary Reserve. Everoze considers that it is unlikely that TSOs in FCR will notably increase the duration of current contracts. Rather, Everoze expects TSOs to consider a separate product for fast-response Primary Reserve with longer contracts as a means to drive down costs and increase deployment of batteries.

- Storage revolution on the mainland, not just in French islands: We have already seen storage deployed in French overseas territories, such as Akuo’s Bardzour PV-Li-ion project in La Réunion or Engie’s Alata project in Corsica. But activity in mainland France has been mainly limited to R&D and pilot projects such as the Ventea SmartGrid project. The UK is undergoing a “battery boom” spanning the full range of transmission-connected, distribution-connected and behind-the-meter deployment. Revenue-stacking is becoming a reality. Our bet is that we’ll start to see storage activities ramp up in metropolitan France sooner rather than later – particularly given EFR’s striking results.

All of which is very exciting – we look forward to the storage revolution ahead!

Any questions or comments, please get in touch.