The current GB energy market design does not work for consumers in a Net Zero future

Published 5 April 2022

In this article by Everoze Partner Nithin Rajavelu, he examines what’s been happening with our energy prices recently and shares his thoughts on why the current GB energy market design doesn’t work for consumers in a Net Zero future.

OK that’s a bold assertion in my title I admit. I am not an energy market nor policy specialist, far from it, but some of the ‘weirdness’ I’ve seen in the energy market dynamics this last year leads me to think “surely there is a better way to do this”.

I’ve got a confession: I’ve been obsessed with my energy prices these last number of months. Come on, who hasn’t, given what’s been happening with our energy markets recently!?

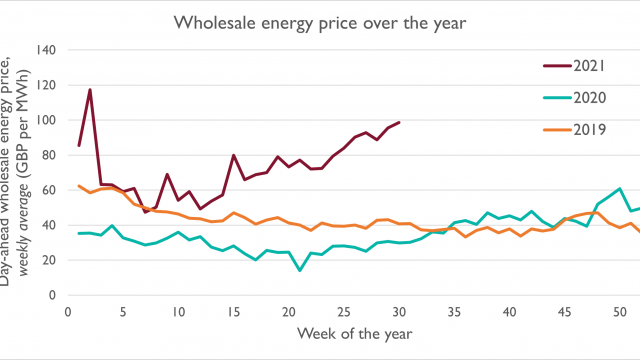

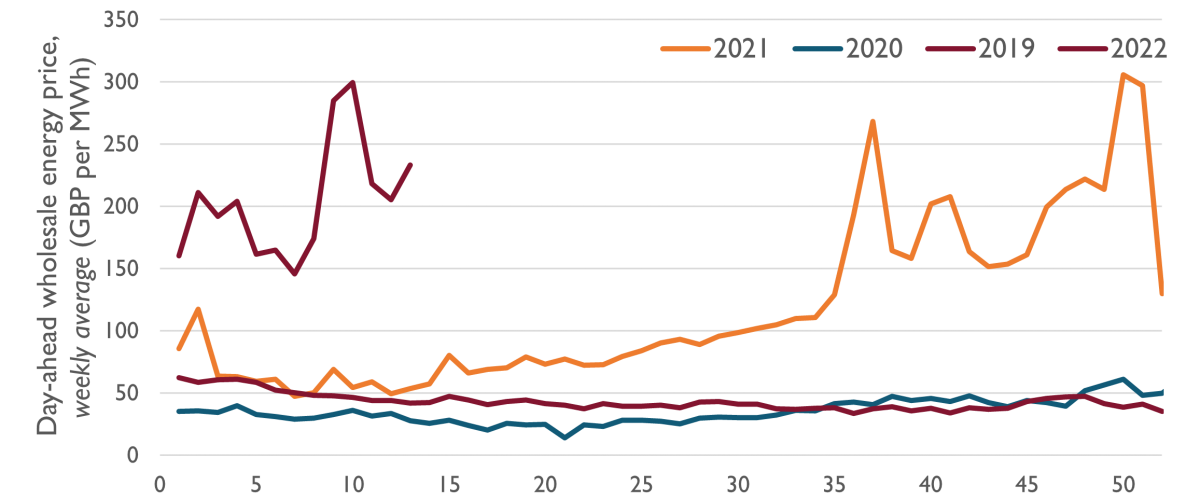

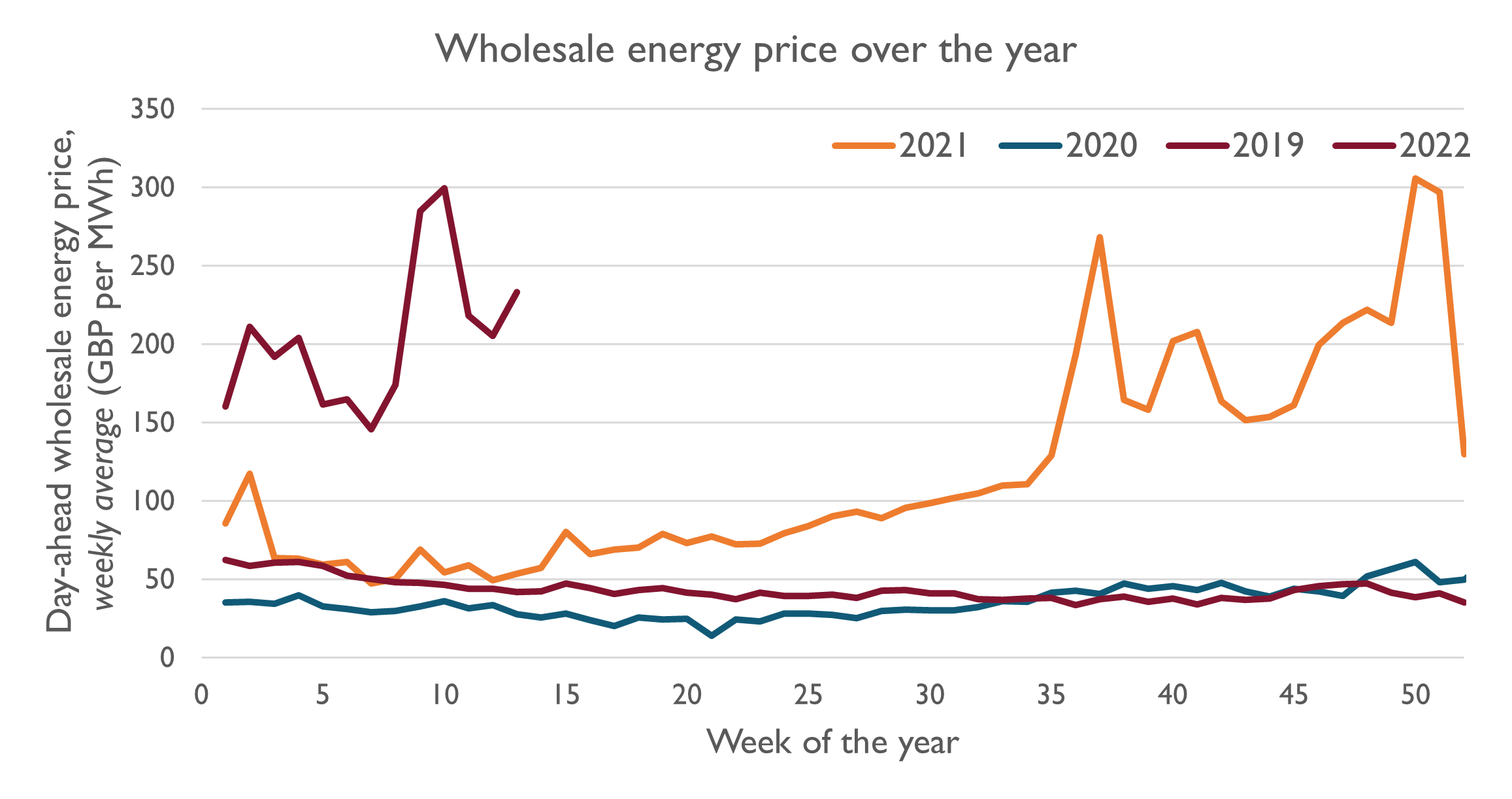

The “historically unprecedented” trend in wholesale prices we’ve seen through the latter half of 2021 and into 2022 continues to break the record sheets. If you’re on a flexible energy tariff like I am and have been feeling the highs and lows (or lack thereof!) in the energy market, you’ll know what I am on about. Now with the increase in the energy price cap from 1 April onwards, all of us are feeling this in our energy bills.

The “historically unprecedented” trend in wholesale prices we’ve seen through the latter half of 2021 and into 2022 continues to break the record sheets. If you’re on a flexible energy tariff like I am and have been feeling the highs and lows (or lack thereof!) in the energy market, you’ll know what I am on about. Now with the increase in the energy price cap from 1 April onwards, all of us are feeling this in our energy bills.

Global gas supplies have been on a squeeze since early 2021, now exacerbated since the invasion of Ukraine. Electricity prices in GB have been driven up as a consequence, because expensive gas generation continues to set the price in the wholesale energy market for the most part. This is in spite of approx. 50 to 60% renewables and nuclear generation in our energy mix.

But what really caught my eye were the days the energy price plummeted to low and even negative prices during some hours of the day. How can we experience negative energy prices and ‘historical highs’ at the same time, sometime even on the same day!? It’s a bit paradoxical, like something out of Lewis Carroll’s mind. I find it hard to wrap my head around this. Can you?

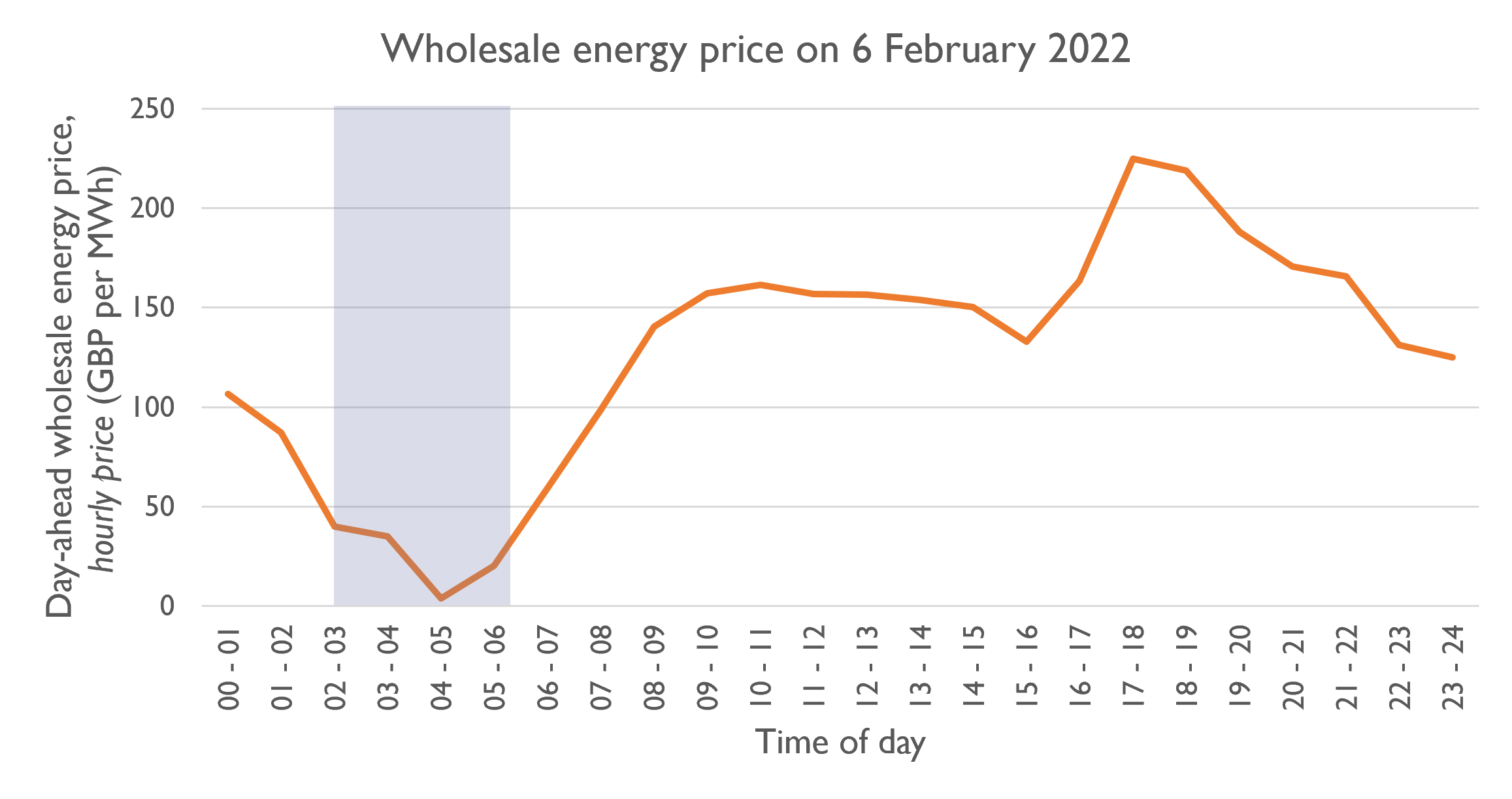

Take the 6th of February as an example.

But first, a quick crash course on the wholesale energy market if you’re wondering how all of this works.

Majority of the energy trades between buyers and sellers of electricity is done bilaterally years up to days in advance of generation through ‘hedges’. Closer to the time, energy is traded via power exchanges in the day-ahead and intra-day ‘spot’ markets. These exchanges operate a ‘pay-as-clear’ mechanism for the day ahead market where the energy price for any 1-hour period is set by the marginal price setter in the merit order.

In other words, if you arrange all the generation volumes for that 1 hour in ascending order of price (GBP per MWh), the most expensive generator needed to meet the forecasted electricity demand sets the price for all generation in that 1 hour.

So even if you have a scenario where 99.9% of demand is met by renewables and other low carbon generation that offer a cheap or even negative price for generation, the last 0.1% met by expensive gas generation still sets the price for all generation in the spot market. If the demand were to drop by 0.1%, the expensive gas generation would not be needed to meet demand and so would be ‘priced out’. The spot price will then be set by the renewable and other low carbon generators at low or even negative levels.

This is just an illustration for how the day ahead market works. But bear in mind that the energy price to the consumer is also heavily influenced by the hedges outside of the spot market.

So, what happened on the 6th of February?

The day-ahead energy price cleared at about £4 per MWh in the early hours of the morning (4-5am) with the price either side of this hour generally being at or less than £40 per MWh for a few hours. As the morning progressed, the price climbed back up to around £150+ per MWh from 9am onwards peaking at £225 per MWh in the evening.

I don’t know the exact market drivers that led to this drop in the early hours of the morning on this day. I expect this is due to reduction in demand on the weekend coupled with increased renewable generation pricing out more expensive gas generation during these few hours. That brought down the clearing price to as low as £4 per MWh. But as demand increased later in the day more expensive gas generation was needed to meet demand which increased prices to £150 to £225 per MWh in the afternoon and evening.

This is more evident during the 1st of January when prices dropped to as low as minus £50 per MWh for a few hours in the morning but climbed back up later in the day to peak at £208 per MWh in the evening.

What does this mean for consumers in a Net Zero world?

Ofgem has reaffirmed its Net Zero commitment to reduce reliance on gas to protect consumers from the volatility of rising gas prices. To clarify, Net Zero does not mean a 100% renewables-powered grid. Gas and other marginal price generation will still be around and will likely continue to set the price. So even with cheaper renewables being built will we as consumers really see the benefit of this in our energy bills?

My suspicion is that the high energy prices we’re experiencing now will continue in some form beyond the current gas supply crunch as our grid continues to decarbonise and the load factor of marginal plants like gas generators decrease.

I do not mean to suggest Net Zero is bad for the consumer, not at all. But what I do think is that our current energy market design is not fit-for-purpose for a Net Zero future, and we need wholesale market reform to support the future we want to create. We need to ensure that the energy market provides the right market signals to incentivise investment in renewables and low carbon flexibility whilst ensuring the consumer interests are protected. The work done by the Energy Systems Catapult for example points in the right direction.

Wholesale market reform is not the only answer here. Options such as passing through the CfD payments from wind farms as savings to UK households as pointed out by my colleague Ben Lock amongst other measures should also be considered.

Ultimately, we need to plan for a Net Zero future that works for us all, and ensure consumers can see the benefits of cheaper renewables and low carbon generation in their energy bills.