Sky’s the limit

As published in PV Magazine International May 2019

Operational assets are aging, with many having not more than five years left to operate within the original setup of 20 years. A wide variety of options are emerging for repowering, and some younger projects are underperforming so badly that they require a strategic rethink long before the original life ends. Everoze’s Ragna Schmidt-Haupt looks at just how realistic extended lifetime assumptions are, and what justifications are needed to underpin a repowering or retrofit business case.

Most middle-aged PV projects were built assuming a 20 to 25 year lifetime. This is partly driven by traditional module warranties’ duration of 12 to 25 years, and the fact that the electricity price was so far off the market no one dared to believe that there was a life after FIT. Lenders, generally more conservative than investors, typically assumed between 15 and 20 years, closely related to the length of the secured tariff. Yet, as PV technology continues to mature, the financial community is stretching its comfort zone by taking more aggressive assumptions on lifetime – or degradation – or both!

With proof of either a secured PPA contract or a sufficient level of predicted electricity market prices in late life, banks may grant an extension of another one to three years beyond a 20 year tariff. Investors are going one step further to boost project valuation by shifting lifetime assumptions up to 30 or even 40 years in financial models. This is mainly driven by the competitiveness of the market and the lack of available assets. Equipment warranties are catching up to some extent, with module manufacturers offering up to 30 years. And appropriately sized inverter maintenance reserve accounts can ensure this key component is underwritten as we move well beyond traditional design lives. Most other items may be wrapped into increasing Opex forecasts beyond the guaranteed tariff period.

In theory, the impact of adding a few extra lines to the financial model after year 20 is diminished to some extent due to the discounting effect on the net present value. However, assuming a simple continued operation – even without any revamping or retrofitting – of another five to ten years of life, the asset value may increase significantly. The augmented value of a full repowering may well extend this further.

A holistic view

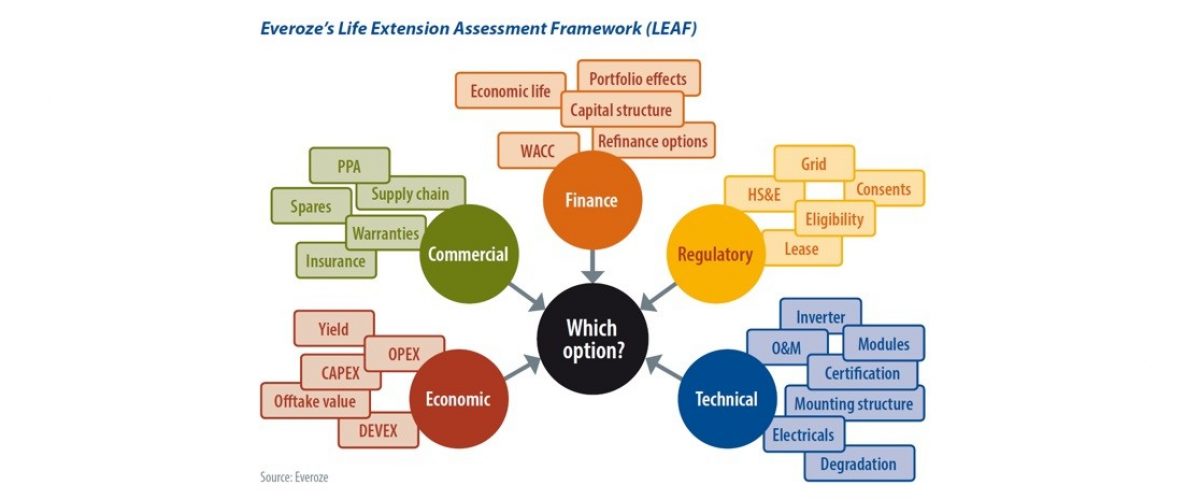

When considering life extension options a holistic view is beneficial, considering at the same time commercial, financial, economic, regulatory, and technical drivers, which are often interrelated.

While the assessment of simply extending the life with no big changes to the status quo is already complex, the investment case of fully repowering a PV asset creates challenges and needs significant resources to be mobilized. However, it can prove to be a major source of uplift. For example, a lightly retrofitted, renegotiated, and refinanced project by MPC built in 2008 increased its revenue by 2% in the first year of operation following refit instead of a previous reduction trend of about 1% per annum. Retrofitting coating onto modules has the potential to boost production further – by up to 2-3% according to DSM. Indirect benefits can be derived from the installation of new software platforms allowing for more efficient predictive maintenance and portfolio harmonizations. Other examples such as switching to string optimizers reduce O&M costs and open up a range of possibilities such as adding energy storage. Finally, replacing old inverters can also help with serial defects post-warranty, which leads us to the next topic.

Warranties, supply chains, and spare parts for key components are essential commercial aspects of the decision matrix on if, when, and how to extend the life of a PV project. With a well-known number of manufacturers having slid into bankruptcy in the past, it is critical to assess the supply chain for availability of spare parts and replacements. Just recently Schneider Electric announced its exit from the utility-scale market. And many old models are not even available for replacement, such as First Solar’s first series.

Another vital component to be considered is the offtake, i.e. types of contract and tariff for the sale of the electricity. While some investors are able to take on some level of merchant risk, others require the security of less flexible, but more reliable corporate PPA contracts. Fully repowered projects may even be eligible to participate in auctions and secure longer-term tariffs.

Finance is more relevant in the case of repowering than for extending life. Refinancing with low cost capital has been a key value driver for retrofits in the past, and very much in the comfort zone of financiers and bankers alike. However, the situation is changing with interest rates on a gradually increasing trajectory in some jurisdictions, potentially impacting the timing for the redevelopment or repowering decision.

Regulatory aspects often present roadblocks for life extension. The most relevant aspects are related to the “holy trinity” of grid-connection, lease agreement, and planning or construction permits. Their respective duration may well differ from the lifetime assumed in the financial model and renegotiation of terms and dismantling clauses or reapprovals for permits can be time-consuming. Repowering of assets is dependent on the regulatory requirements of each country. The most flexible market is currently Italy, as it allows for system improvements with dedicated repowering directives.

Economic drivers are the most visible of all aspects in the financial model. The advantage of solar PV compared to other renewable technologies, is the high predictability of the behavior of the operational plant at a known site. The uncertainties mainly lie in longterm degradation and Opex assumptions. For a thorough sizing of the operational expenditures it is essential to consider failure and replacement rates for inverters, transformers, PV panels, and mounting structure.

Eyes on the future

With project lifetimes extending towards the 40 year mark, it is important to keep an eye on a number of hypotheses that have a potentially significant impact on the valuation. Repowering has many embedded benefits beyond boosting returns, including new warranty terms, compliance with a new regulatory context, and the possibility to correct mistakes in the original design. Despite this, asset management teams seem still reluctant to tackle this topic, especially the ones embedded into pure financial plays without any development experience, and because their investment mandate is limited to the original financial model. For asset owners keen to make the most out of their grid connection, planning consent, and lease agreements, extension and redevelopment will sooner or later be put on the table. Despite the lack of a feeding frenzy at present, there are plenty of reasons to expect that these topics will ultimately lead to a tempting feast for savvy owners.