Latest capacity market data reveals clues on the future of UK storage

Published October 2016

The Capacity Market Register T-4 2016 is out. Everoze plays detective on the data to solve the mystery of the future of UK battery storage.

Something odd happened last Friday 14th Oct.

The Energy & Climate Change Commission (ECCC) published a report that reached a grim assessment on storage’s ability to participate in the Capacity Market (CM). It urged Government to “review the outdated Capacity Market rules and regulations in relation to storage”, bemoaning the poor track record of past auctions in bringing forward battery projects.

Yet just hours after the ECCC publication, the Capacity Market Register T-4 2016 was released. It was a typically clunky Excel sheet full of obfuscatory acronyms. But one thing was obvious straight up: it contained a bucket-load of batteries.

This was all very mysterious: how could the ECCC report be so damning, and yet the CM Register contain so many battery projects? It didn’t seem to add up. The mystery matters because there’s serious money to be made here: word on the street is that this year’s CM auction will clear well above the £18k/MW prices seen in December 2015.

Time for some detective work. As a provider of technical due diligence, the Everoze team is used to ploughing through project datarooms – but today we decided to turn our magnifying glasses to the CM Register instead. We hunted down and stripped out site duplicates. We trawled through the Companies House database to trace storage SPVs back to parent companies. We scrutinised CM project details to match them to Enhanced Frequency Response (EFR) bids – even deciphering where some companies had ‘piggybacked’ on the EFR prequalification of another party. Whilst we might have made the wrong inference here and there, we think we’ve got one step closer to solving the mystery of the future of UK energy storage.

Here’s what we found.

The battery bonanza continues

First, the headlines:

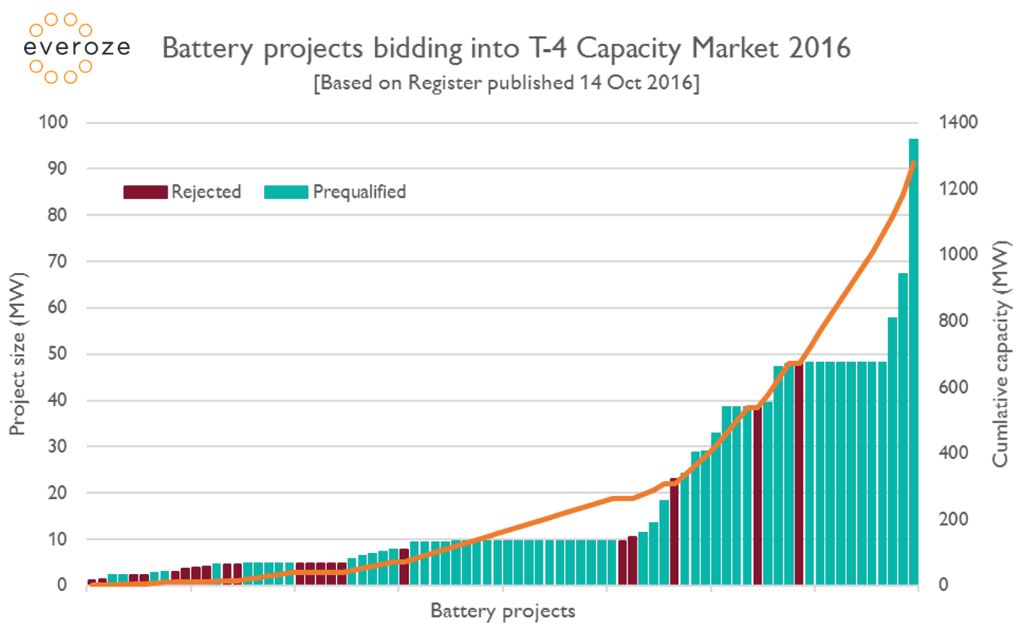

- A whopping 1.47 GW battery storage sought CM qualification, of which 87% prequalified – with a large tranche of sub-10MW projects in particular. Check out this chart:

- 52% of the battery projects (by MW) seeking CM qualification did not bid into EFR, meaning that there’s over 750MW of new battery storage projects in the UK pipeline on top of what we saw in the landmark EFR tender.

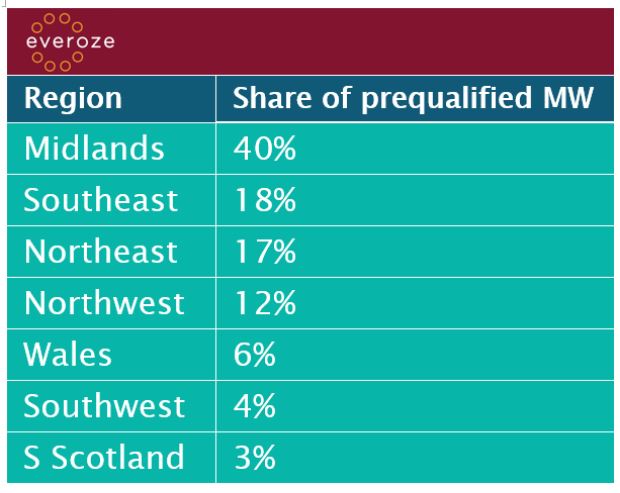

- The Midlands is the place to be, offering the sweet spot between ability to secure grid connection and palatable charges for using the grid. Scotland barely gets a look-in:

The revenue strategies of EFR winners are diverging

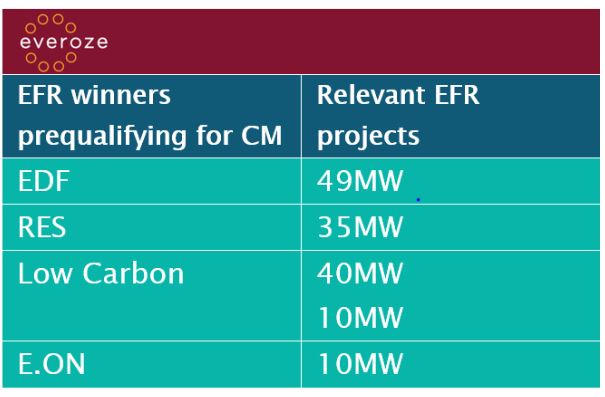

Perhaps most interestingly, the CM Register reveals that the EFR winners are adopting different revenue stacking strategies. In our latest blog, we highlighted a divergence amongst the winners in approach to stacking EFR with triads. Now we’re seeing a split on CM strategy too.

EDF, RES, Low Carbon and E.ON all prequalified their EFR projects for the CM. And the other EFR winners? One had their CM application rejected, and the remaining two don’t seem to have applied.

The players in this Table will now be seeking to urgently resolve the revenue interface risk between EFR and the CM. The EFR contract provides a mere one-sentence reassurance that the two revenue streams can be stacked, backed up only by high-level guidance in a Q&A document.

Playing detective: the grand reveal

To sum up: yes, the ECCC report is right to highlight regulatory headaches hindering storage’s participation in the CM. But in one sense, it is already out-of-date: CM prequalification data released the very same day shows that developers are bulldozing ahead regardless.

Everoze will conduct further detective work once the full CM auction results come out. Till then – any questions or comments, please contact us on contact@everoze.com