What?! £7/MW/hr for EFR storage? Explain!

Published |September 2016

We explain how the low prices in the UK’s landmark tender were achieved – and what this means for the future of storage.

We’d been waiting for weeks: yes, last Friday was EFR results day. We were told that all would be revealed at 1pm; though of course, that didn’t stop us from obsessively hitting “Ctrl+F5” to refresh the EFR webpage at 5 minute intervals all morning. As if to tease us, a Press Release was issued early stating that the results were already published on the National Grid website (they weren’t).

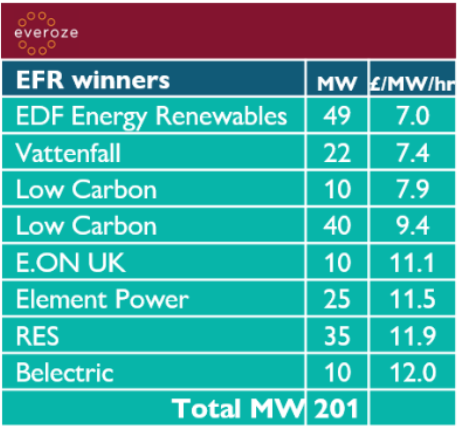

But at last, the clock struck One and the results were in: eight contracts awarded, at £7-12/MW/hr.

The question on everyone’s gibbering lips: how could prices sink that low? It seemed paradoxical: National Grid had said months ago that EFR has greater value than other services, so how could prices fall lower than what we see for Firm Frequency Response (FFR)? As a sign of just how topsy-turvy the pricing was, the aggregators – who specialise in understanding ancillary services pricing – all failed to bag a contract.

At Everoze, we were expecting something dramatic; some of you will have seen our blog earlier this month predicting that “people are going to be really shocked by quite how low EFR prices go”. I’ll be honest though: the bottom range of the bids even caught us by surprise.

Perhaps it shouldn’t have. Here are our reflections, now the dust has settled.

Financing drivers help explain why prices went so low

Within minutes of the results being published, theories behind the low prices were flying through via email, phone and social media. Explanations included:

- Strategic play: Some winners were accepting below-normal returns to gain first mover advantage

- Future revenue: The winners took a strong view on post year 4 revenues

- Access to cheap capital: Utilities had muscled in with their access to cheap capital

- Site selection: Winning projects had picked sites with inherent cost advantages.

There is some truth in all of the above. But none of it quite explains how EFR could sink below FFR. And here, one point has been hugely overlooked: EFR and FFR are a false comparison due to their different contract lengths.

As a due diligence provider for financiers, Everoze has been harping on for a while about how longer contracts drive down financing cost. EFR is attractive because it offers four year contracts, which contrasts the higher merchant risk entailed by FFR. Whilst four years is shorter than it should be, it’s better than the FFR alternative. EFR bidders went in hard because they understood that in the UK’s complex revenue-stacking landscape, a four-year contract helps get financiers on board – whether that’s external project financiers, or internal Investment Committees.

This tender has implications beyond just the winning projects

But let’s not fixate on the prices too much. Because whilst everyone’s trying to get their heads around how the winning bidders did it, we think there are now three wider implications to watch out for.

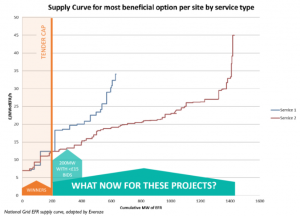

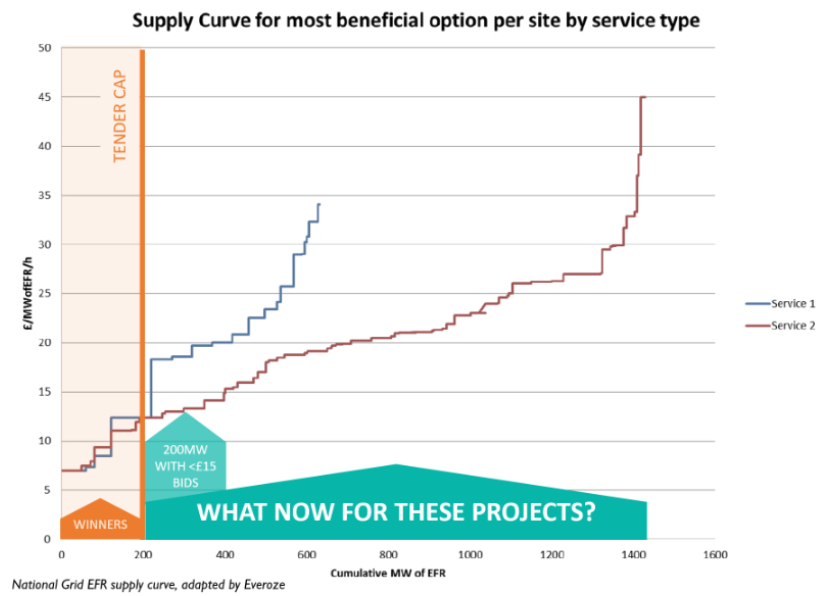

- The unsuccessful bidders: There is well over 1GW of ready-to-go storage projects which did not receive EFR contracts. Of these, 200MW look particularly attractive, coming in with sub £15 bids [see chart below]. What will happen to these projects now? Some unlucky bidders might be scared off by the low prices, some might wait patiently for the next EFR tender – and others will now explore FFR. Watch this space.

- System operators abroad: National Grid claims this tender has saved £200mn compared with the cost of alternative action. That’s a bargain that other System Operators cannot ignore. Expect to see similar tenders replicated abroad.

- Ofgem: The publication of Ofgem’s Embedded Benefits letter in July challenging the future of triads caused true “triads and tribulation”, splitting EFR bidders in two. Six chose to withdraw projects that relied upon triads as a supplementary revenue stream. Meanwhile others – including one winning bidder – held firm, continuing to assume triads within their revenue stack. All this further ramps up pressure on Ofgem to swiftly clarify the regulatory outlook.

What a crazy few months…

The EFR pilot was bigged up as a landmark tender for storage and these results have lived up to the hype. We look forward to hearing your views – feel free to post comments below.

But for now, please excuse me: I’ve got an F5 key that needs fixing.