I was wrong: batteries don’t need longer contracts

Published November 2016

Some financiers are determined to back storage, regardless of contract length. But there are trade-offs: are we prepared to accept a battery monoculture and higher costs?

Oops.

This is all a little embarrassing.

You see, I’ve been talking for ages about how storage needs longer contracts from National Grid and others to get financed. The evidence is here, here and here. My rationale was simple: short contracts create a real headache for investors and banks in valuing later life project revenues, particularly in a new market with high regulatory uncertainty. I was worried this would leave storage as an elite playground for large utilities who could fund projects on balance sheet, squeezing out all competition from independent developers.

Turns out I was wrong.

Thanks to innovation from forward-thinking players, the financing environment for storage is looking pretty darn competitive. Whilst many investors (and particularly lenders) remain hesitant, the most agile funds are getting comfortable with revenue myopia.

There are now – finally – real projects on the table with compelling revenue strategies, including behind-the-meter portfolios. And investors are fighting between them. From Everoze’s work as Technical Advisor, it’s clear there’s going to be some meaty transactions kicking off pretty soon.

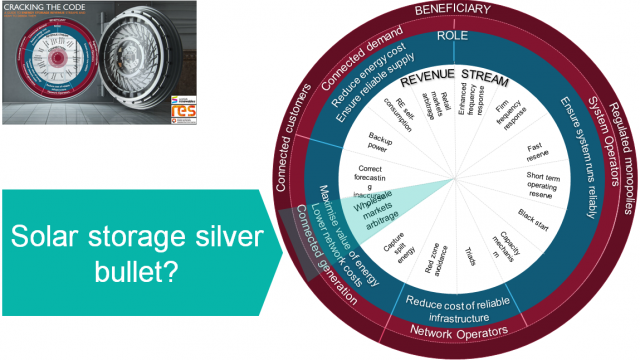

Towards flexibility hubs

And, in chewing through my humble pie, this got me thinking – and thinking quite differently. Perhaps we need to stop obsessing about securing multi-year contracts, and think more about storage as a ‘flexibility hub’, participating on a merchant platform for trading. Perhaps longer-term, it’s less about locking down the revenues, and more about hopping between different revenues, bolting on extra capacity as needed. Perhaps it’s about greater creativity in revenue stacking – for instance, exploiting diurnal and seasonal trends in frequency response value to eke out more value.

In this ‘flexibility hub’ future, storage will serve a range of counterparties. Some will be well-known and trusted – like the distribution system operator. Others will be total strangers, as blockchain technology enables anonymous peer-to-peer trading. You might rent out your battery to National Grid for one hour, and to your neighbour for the next. Storage as a service becomes the norm.

Incidentally, this seems to be what BEIS and Ofgem (the UK’s policymaker and regulator) are hoping for when they talk about ‘flexibility trading/optimisation platforms’ in their latest Call for Evidence.

Beware: battery monoculture, and higher costs

But before we all merrily skip along to Silicon Valley, a dose of realism: transitioning to flexibility hubs will be a real slog. It’s easy to splurge out on tech buzzwords, but delivering on the vision will need both regulatory reform and a huge reserve of private sector grit to make it happen. Big-thinking strategists tend to gloss over these ‘details’ – but anybody battling through real-life revenue interface risk complexities on pioneering storage projects knows how tough the path ahead will be.

And, assuming the barriers are surmountable, ditching multi-year contracts in favour of the pure merchant route brings two big drawbacks:

1. Super-short contracts mean a battery monoculture: Goodbye flywheels. Goodbye pumped hydro. Goodbye compressed air. Short contracts might theoretically be technology neutral, but the reality is that revenue short-termism favours storage assets with short lifespans and/or low CapEx requirements. In a nutshell: batteries. Ok, I’m exaggerating a bit – but anybody challenging this broad conclusion should check out the current policy debate on introducing a cap-and-floor regime for pumped hydro.

2. Short contracts mean more expensive projects – due to higher financing costs: Although banks can generally get comfortable with availability-based payments such as EFR, they’ll tend to only lend against contracted revenues – and fact is, if those contracted revenues are four years or less, debt will struggle to be competitive. This means that projects will largely be equity financed – which makes financing costs higher than would otherwise be the case.

Hands up: I was wrong

So I was wrong: we don’t need longer contracts. 2-4 years is enough to whet the appetite of the most agile investors. But’s let’s be honest about the trade-offs. Shorter contracts mean a battery monoculture, and more expensive, equity-dominated projects.

Is this the price we must pay to realise our high-tech, flexibility hub utopia? I look forward to reading your comments… Please send your comments to contact@everoze.com